Crude Oil Futures Outlook

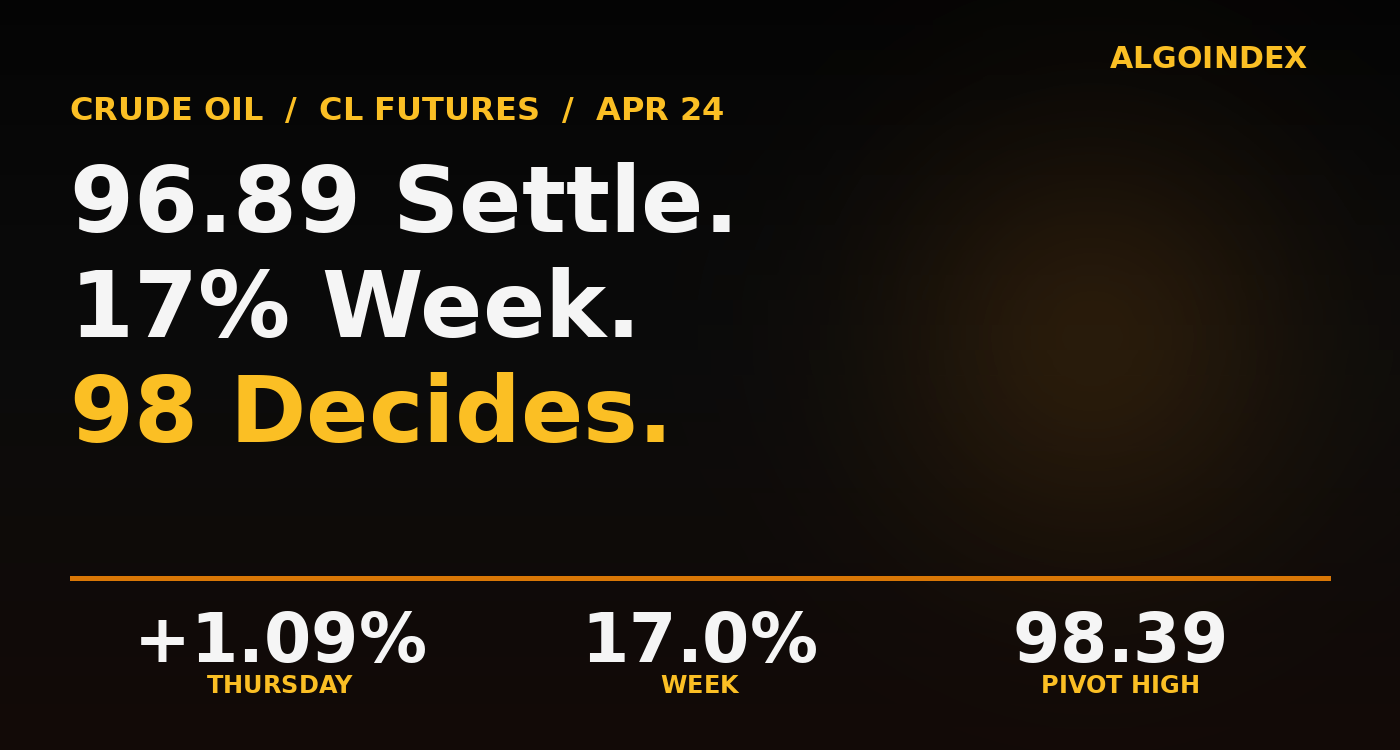

A 96.89 settle, a 17 percent week, and a three-dollar decision pocket into Friday’s close.

At 4:02 PM New York time on Thursday, the June WTI contract settled at 96.89 and printed its highest daily close since the April 7 supply flood capitulation. The daily bar was small but honest: open 96.62, high 97.35, low 95.88, a session that spent its final hour in the upper third of the range. The intraday story was cleaner than the number suggests. A Persian Gulf wire item on the continued Strait of Hormuz closure crossed terminals in the 2:30 ET hour, and the front contract lifted from 96.60 to the 97.35 intraday high in the next twenty minutes of flow.

That settle now sits inside a three-dollar decision pocket defined by the 98.39 weekly pivot high and the 95.88 session low. Friday’s close will mark the end of a week that opened at 88.15 and could close above 97, a roughly 17 percent move that reverses most of the April 7 supply flood crash and takes the front month back above every moving average from the 5-day through the 200-day stack. It is one of the most violent weekly recoveries in the last twelve months, and, importantly, it has happened without a durable shift in the forward curve. The June-July calendar spread is flat to mild contango, a configuration that says the physical market has absorbed the Hormuz premium but has not yet moved into the backwardation that would confirm durable tightness.

The Sequence From 78.97

The technical structure is where the bull case lives. Price has printed a third consecutive higher-low off the 78.97 one-month swing low from April 16. The daily moving average stack reads 5-day at 92.59, 20-day at 92.17, 50-day at 83.44, 100-day at 71.33, 200-day at 66.24. A 5-day sitting 7 percent above the 50-day and a 50-day 26 percent above the 200-day is a post-capitulation configuration, not a mid-cycle trend. The 5-day has accelerated 17.5 percent over the prior period, an extreme reading that tells you the short horizon is stretched even while the larger structure is still catching up.

Oscillators are the tell. RSI-9 reads 61.12, RSI-14 at 59.01, RSI-20 at 58.81, all sitting in a 58 to 61 band that says trending-up without yet hitting the 70 overbought line. Stochastics run hotter: 9-day Raw at 93.10 percent, 14-day Raw at 81.44 percent with %K at 73.50. RSI in the mid-60s while Stochastics push the upper 80s is a late-recovery signal that typically resolves with a pullback to mean before the next leg. ADX on the 20-day frame reads 32.25 with positive directional index at 24.27 against negative at 18.59, confirming an active trend and arguing against calling the top here. The multi-indicator composite scored 80 percent BUY on the next-session projection.

Historic volatility on the 14-day frame reads 82 percent annualized, the highest print in more than a year. This is not a market where a tight stop survives. Any CL position needs a minimum 75 to 100 cent buffer and sizing should be one-third to one-half of an equivalent ES-risk position.

Hormuz Over Fundamentals

Crude has no options-market proxy the way gold gets through GLD and the Nasdaq gets through QQQ. USO is structurally degraded by contango drag and its options are too thin to read. That leaves the physical-market macro stack doing the work, and right now the stack is weird.

The prior EIA Weekly Petroleum Status Report came in at plus 1.925 million barrels, a modest build. The industry preview released Tuesday showed the same direction. On paper, a build at 96 dollar crude should have pressured price. It did not. The Hormuz flow overrode the inventory read entirely, the first tell that this is a geopolitical-premium week rather than a supply-demand week.

Positioning Read

Money managers still net short from the April crash. Commercial hedgers net long. Open interest rising through the week on the June contract. The 3:30 PM ET Friday positioning report will show data through Tuesday April 21, and a sharper net-short-to-neutral shift in that print reinforces the bull case into Monday.

Then the curve. A mild contango says the physical market still doubts durable tightness. If Hormuz stays closed into a second week and the curve begins to bend toward backwardation, the move from here is not a small one. If the headline resolves over the weekend, the premium compresses fast.

Cross-asset confirms a commodity-specific story rather than a broad risk-off event. Dollar Index at 98.81 is quiet. VIX at 19.30 ticked up 2.06 percent. ES closed 0.19 percent higher at 7,156.50. Gold settled slightly softer at 4,712, a modest divergence from crude’s bullish day that tells you the safe-haven bid is being parked in the dollar and Treasuries, not across the commodity complex. This is a single-instrument repricing.

The 98 Decision Zone

Above the 97.35 Thursday session high, the next structural wall is dense. The 98.39 weekly pivot high, the 98.52 computed target, the 98.53 Fib 1.618 extension from the 1-hour structure, and the 98.73 Pivot R1 all converge into a tight supply pocket. That zone will take meaningful flow to break on first approach. Above it, the 99.91 Price 1 Standard Deviation resistance and the round 100 handle provide a second reaction zone. The extended ceiling lives at 101.17 (one-month high), 101.59 (Price 2 StdDev), and 101.60 (Pivot R2), a triple-confluence pocket that would represent a blow-off extension target on a Hormuz escalation headline.

Support is tiered and shallow. Immediate demand sits at 96.18 prior-session point of control and 96.02 at the 18-day moving average stall line. Below that, 95.88 (Thursday low), 95.85 (Wednesday close), and 95.51 (daily Pivot Point) form a three-tick shelf bulls need to defend. Breaking 95.51 opens 94.51, then the deeper value pocket at 92.95 to 92.64 where a 9-day moving average, the prior-day low, a Fib 38.2 retracement, and Pivot S1 all converge. A clean break below 94.50 on the daily close negates the swing-long thesis.

Primary Setup

Long on a controlled pullback into 95.80 to 96.25, stop at 95.60.

Targets: 97.35 (T1) â 98.53 (T2, 1H Fib 1.618 with weekly pivot high) â 101.17 (runner, one-month high if Hormuz premium sustains).

Risk/reward runs roughly 1:2.5 to T1, 1:4.8 to T2, 1:9.4 to the extended. Four live invalidators: OPEC supply-release announcement, Hormuz-reopens headline, DXY break through 99.50, or a risk-off move that pushes VIX above 22.

The Weekend Gap Problem

There is no EIA print Friday, no OPEC ministerial statement, no FOMC speaker. The first-order US input is the University of Michigan Sentiment Final at 10:00 ET with the one-year and five-year inflation final reads attached, 4.8 percent and 3.4 percent expected respectively. Any upside surprise on long-run inflation expectations firms the dollar and presses crude mildly from the DXY channel. Secondary risk comes from the weekly positioning report at 3:30 PM ET.

The larger structural problem for a Friday long is the weekend gap risk. A closed Strait of Hormuz heading into a weekend is the type of condition that historically produces Sunday-evening opening gaps of 2 to 5 percent in either direction. Position sizing into the Friday electronic close needs to respect that, which in practice means reducing size or exiting swing exposure before the 5:00 PM close rather than carrying a full position through to the Monday reopen. Yesterday’s session closed at 92.96 and gave back ground overnight to 92.30 before the London bid returned. A similar air pocket on Sunday night at 97 would be a five-dollar event.

The June contract is priced for more than a supply-demand story and less than a confirmed supply shock. Friday’s close will start to decide which one.

Join the Discussion

Connect with other ES futures and SPY options traders. Share setups, discuss levels, and get real-time market insights from our community.

Join AlgoIndex Trading Community