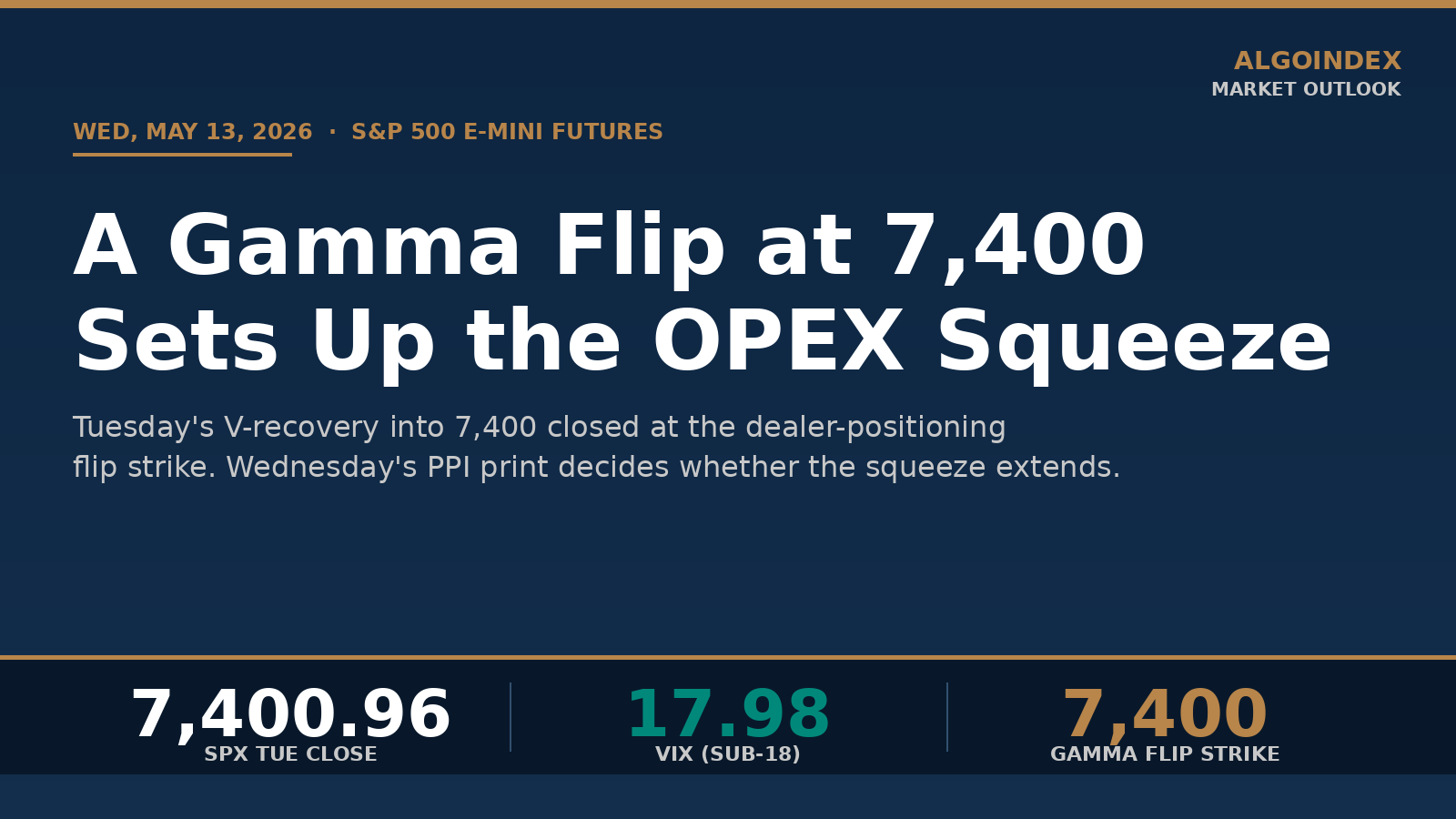

At 4:00 PM Tuesday, S&P 500 E-mini futures settled at 7,400.96, within a quarter point of the strike where dealer positioning had just rotated from shock-absorber to acceleration switch. The number itself looked unremarkable, a red close worth 0.16%. The structural change underneath did not.

A 3.8% CPI print at 8:30 ET that morning, fifty basis points hot in a single month, had broken the disinflation story most desks had been carrying since March. ES gapped lower into the open, then carved a 71-point trough by 10:45 ET. From 13:00 forward, what looked like an organic recovery was something else entirely: cumulative options-delta data showed roughly nine billion dollars of mechanical call-buying flowing through dealer hedge desks in the afternoon, and the V-recovery into the 7,400 zone closed at the same strike where the gamma profile flipped from positive to negative.

That recovery is the setup for Wednesday, not yesterday's headline. With dealer positioning now negative at 7,400, every move above that strike requires the same hedge desks to buy more spot to stay neutral, which amplifies upside. Every move below removes the buy-side hedging pressure and lets gravity do its work. ES opened the overnight session +9 points at 7,435.50, oil cooled below $101, and the 30-day implied volatility reading slipped under 18 for the first time in a week. The mechanical setup favors a grind higher into Friday's monthly options expiration, with two specific lower-bound triggers that would invalidate the bullish read.

The mechanical recovery that built the setup

Tuesday's afternoon move was not bottom-fishing. Real-time hedging-flow readings showed the typical post-CPI hesitation through 11:00 to 13:00 ET, then a sharp directional rotation as institutional call buyers pressed the bid. The nine-billion-dollar swing in cumulative delta did not reflect a change in macro view about CPI. It reflected mechanical flow into specific Friday-expiration strikes that forced dealers short those calls to hedge by buying the underlying.

The asymmetry here matters because realized volatility on Tuesday came in at 97 basis points against an implied 80, meaning the option market underpriced the day's move. Future implied volatility crashed afterward (current 30-day expectations dropped to 17.98 by Wednesday's open), but the volatility-of-volatility reading held steady at 99, which is still in the upper half of the normal range. That combination, near-term vol crushed but forward vol-of-vol elevated, is consistent with a market expecting continued suppression through the end of the week, then expansion potential after Wednesday May 20 when chip-sector earnings hit.

The semiconductor complex got the worst of the CPI shock. The chip-sector ETF lost 2.61% on the session, the Korean equity proxy dropped 7.44%, and the 3x semiconductor product gave back 9.40%. Pre-positioned put buyers in the names that lead the chip cycle did the cleanup work the index itself avoided. The same setup that gave us a 7,183 rejection in late April when Iran headlines cascaded through the chip names is the one institutional desks now use to hedge the inflation-shock variant of the same risk.

What the 7,400 flip actually changes

Before Tuesday's close, dealers held positive gamma across the 7,300 to 7,500 strike concentration, which meant intraday moves got absorbed and prices tended to mean-revert toward the larger gamma strike. After Tuesday's close, the 7,400 strike rotated to negative gamma, which inverts the mechanic. Above 7,400, dealers are now short calls and forced to buy spot as price rises. Below 7,400, the same dealers no longer need to defend the strike with hedging buys, and put-side hedging dynamics begin to compound any selling.

That structural change is the single most important variable for Wednesday's session. It is also the reason the line between bullish-grind and bearish-cascade sits exactly at the same number that closed yesterday's print.

Six confluence zones map the day. Upper resistance lives at 7,450 to 7,454 cash, where computed pivot levels intersect with the upper-band options-flow ceiling. Mid resistance sits at 7,420 to 7,428. The flip strike at 7,400 cash is the gravitational center. First support is 7,383 to 7,390 cash. Major support, where most institutional defense usually appears, is 7,350 to 7,357 cash. The structural lower pivot at 7,286 to 7,300 cash is the line where the bullish-into-OPEX framework actually breaks.

Wednesday's three real setups

The decision matrix at 9:45 ET, after the opening 15-minute window has set the intraday range, is short. ES opening between 7,430 and 7,445 with implied volatility under 18.20 fires the long-continuation trade. Entry sits in the 7,427 to 7,435 zone, stop at 7,415, first target at 7,450 (the upper-resistance confluence of options-flow data and computed pivot levels), second at 7,468, third at 7,478. Risk-to-reward runs 1:1.9, 1:2.8, and 1:4.3 across the three targets.

ES opening below 7,415 with volatility expanding above 18.40 fires the opposite trade. The negative-gamma profile would then work against the rally, with the cascade running first to 7,393 (back into Tuesday's range), then 7,373, then 7,335. Stop sits at 7,432. The counter-trend mean-reversion play at 7,470 to 7,478 only fires on a clean rejection candle with volatility re-expansion, and that one carries the lowest conviction of the three because it argues against the broader options-flow setup into Friday.

There is no first-tier US data release Wednesday on the order of FOMC, CPI, payrolls, or core PCE, which means our standard 15-to-30-minute post-release waiting requirement does not apply. That said, the catalyst stack is heavier than it looks at first glance. Our performance methodology documents how we filter waiting-window rules per data tier.

The catalyst stack behind the bigger setup

Producer prices for April land at 8:30 ET. The print is upstream of consumer prices, and after Tuesday's CPI shock the market will read PPI as the second look at the same inflation question. A cool number partly rebuilds the disinflation story; a hot number compounds the damage and threatens the bullish-into-OPEX setup directly. Crude oil inventories follow at 10:30 ET, relevant precisely because oil cooling below $101 overnight is one of the inputs supporting the broader vol-suppression read. A US 30-year Treasury auction at midday and remarks from the European Central Bank president at 14:30 ET round out the macro slate. Two single-name earnings bookend the session: Alibaba reports Q4 at 5:30 ET pre-market for a China-consumer read, and Cisco reports Q3 at 16:05 ET post-close for a networking and AI-infrastructure read. The Trump-Xi bilateral meeting carries over from earlier in the week as the binary headline risk that does not respect any calendar.

The week's structural pivot is Friday's monthly options expiration, which is when the gamma profile rolls and the suppression mechanic that has held volatility low for two weeks finally releases. Real-time hedging-flow data points to continued equity support and volatility compression through Friday, then a transition into the following week as Wednesday May 20 brings a chip-sector earnings event that typically resets the broader index volatility expectation. The same dealer-positioning framework set up the 7,232 call-wall fade we mapped pre-FOMC in late April, only this time the friction strike is 7,400 and the magnet is OPEX rather than a Fed meeting.

The most likely path through Wednesday, weighted at roughly 45%, is a steady grind from the 7,435 overnight level toward the 7,450 resistance confluence, with extension toward 7,468 if semiconductor leadership participates. A 30% probability sits with a chop range between 7,415 and 7,450 as mid-week digestion takes over with PPI absorbed into the price. Mean-reversion lower toward 7,393 then 7,373 carries roughly 15%, and the tail outcomes that cross 7,290 (the structural lower pivot) sit at roughly 10%.

The strikes that matter Wednesday are not retail moving averages or daily pivots. They are the levels where a few hundred thousand contracts of dealer hedging flow change direction.

AlgoIndex turns this same level work into automated entries, sizing, and exits across ES, NQ, GC, and CL.

View pricingFoundational guides

New to S&P 500 futures? Start with What Are ES Futures, the ES, NQ, MES & MNQ point value and contract specs, gamma exposure (GEX) explained, and market internals: TICK, ADD, VOLD and VIX.