Frequently Asked Questions

Options flow analysis tracks institutional buying and selling of options contracts in real-time. For ES futures traders, monitoring SPX options flow reveals where large participants are placing directional bets, hedging risk, or building positions – often signaling price pivots before they show up on the futures chart.

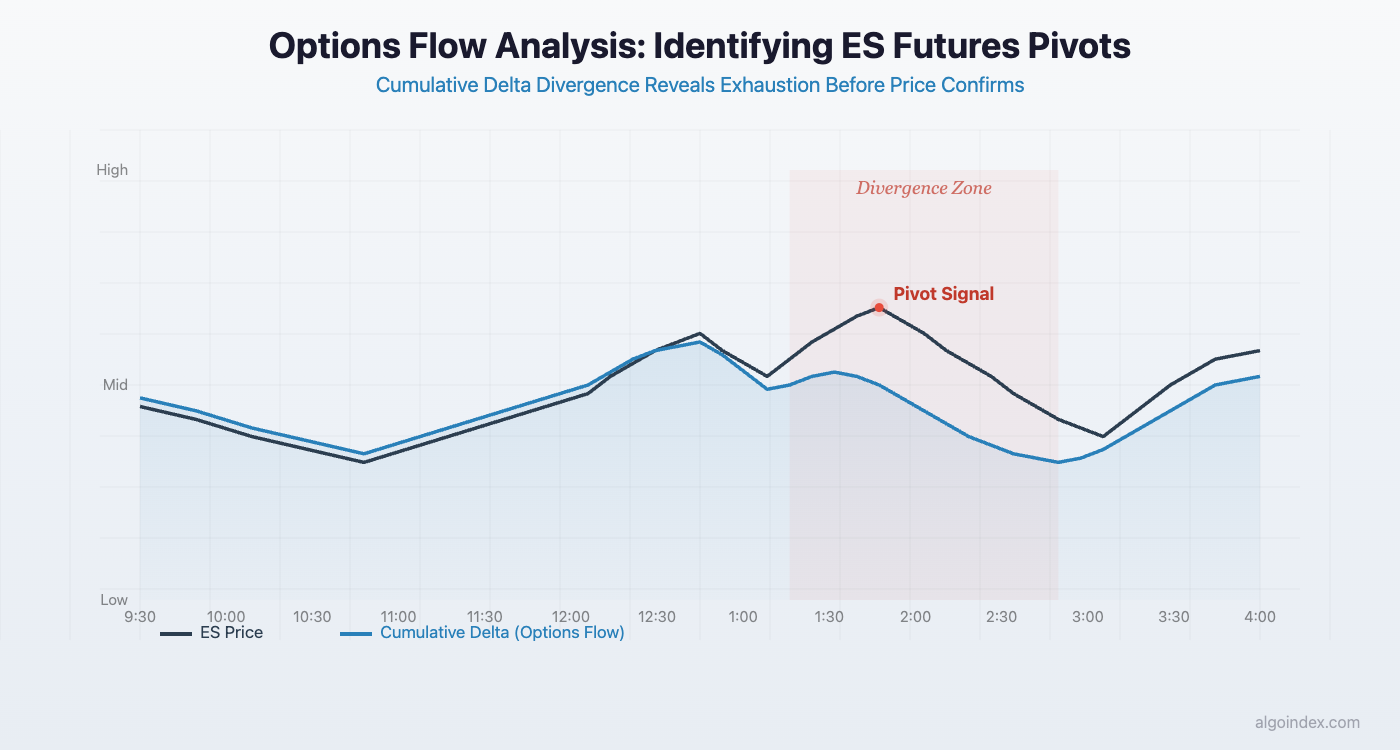

real-time hedging flow (Hedging Impact Real-time Overlay) tracks cumulative customer delta from options trades during regular trading hours. When real-time hedging flow diverges from price action – for example, real-time hedging flow flattening while ES keeps rising – it signals that options flow is exhausting, and a reversal is likely forming. This divergence at key gamma levels provides the highest-conviction pivot signals.

0DTE (zero days to expiration) flow represents same-day options trades that are highly reactive and short-term – these generate large immediate dealer hedging impacts but are prone to reversal. Longer-dated flow (weekly, monthly expirations) represents more deliberate institutional positioning with higher conviction and more stable price effects.

Options flow is most reliable during the New York AM session (9:30-11:30 ET) when institutional volume peaks, and during power hour (3:00-4:00 ET) when end-of-day positioning accelerates. Flow signals are less reliable during lunch hours (12:00-1:30 ET) due to lower volume, and should not be used outside regular trading hours.

Join the Discussion

Connect with other ES futures and SPY options traders. Share setups, discuss levels, and get real-time market insights from our community.

Join AlgoIndex Trading Community