The setup that defines tomorrow is not a chart pattern. It is a calendar.

At 2:00 PM ET on Wednesday May 20, 2026, the Federal Reserve releases the minutes from its most recent FOMC meeting. Two hours and twenty minutes later, at approximately 4:20 PM ET, Nvidia reports Q1 2027 earnings with an options-implied move of 6 percent in either direction. These are not adjacent events. They are stacked back to back on a single trading session, with the largest single-name binary in US equities arriving exactly when the macro liquidity backdrop is at its most fragile in months.

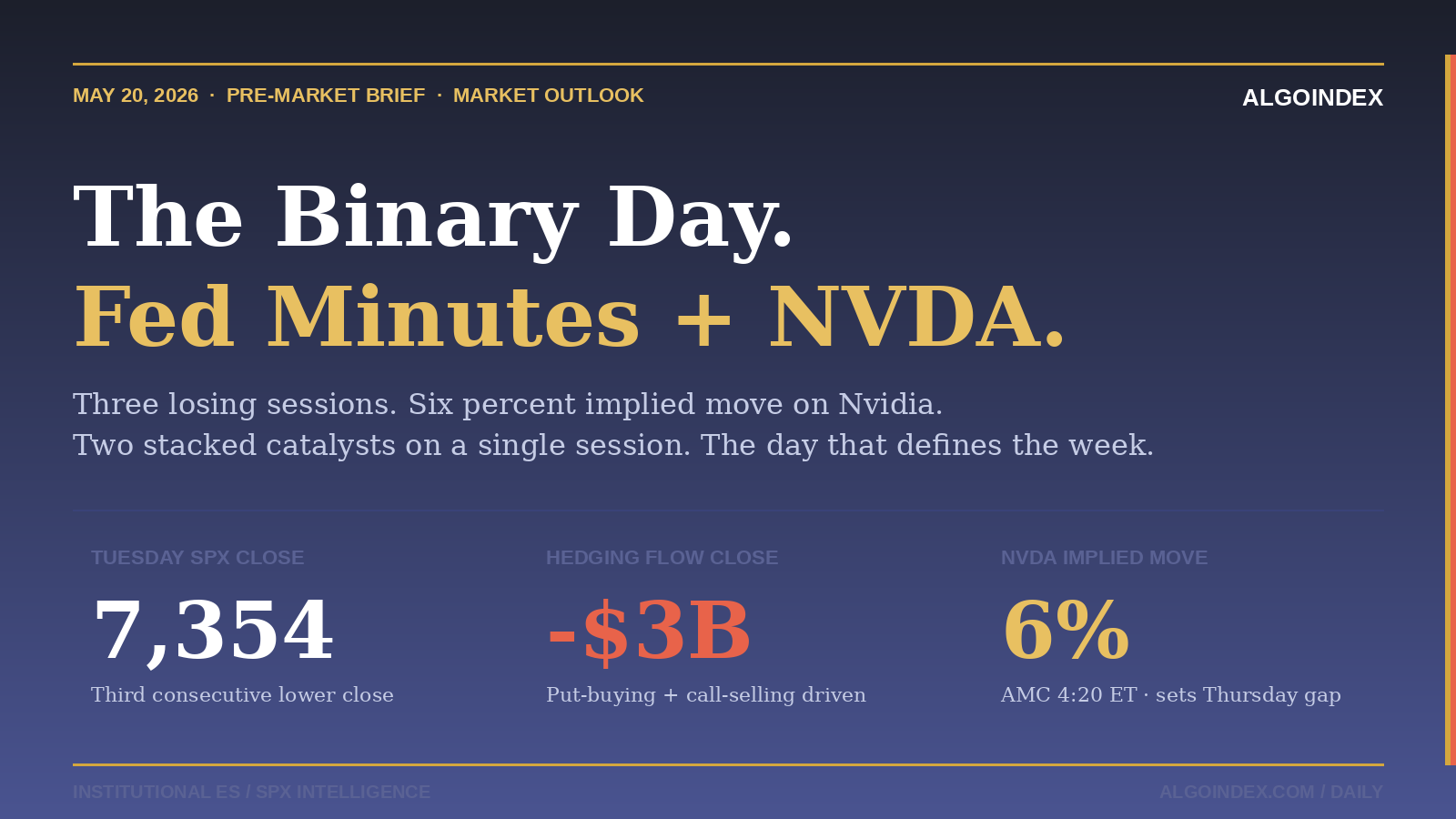

Tuesday closed at SPX 7,354.18, down 0.67 percent, the third consecutive losing session. The index now sits structurally below the dealer-positioning bull/bear line at 7,390 and approximately 25 points above the 0DTE put support at 7,330 that is anchored by an 8,000-lot put spread engineered into Wednesday's expiration. Real-time hedging flow finished the session at minus three billion dollars, the lowest read of the day, with approximately two billion of put buying and one billion of call selling driving the print. The Treasury bear-steepener continued, with the 10-year yielding 4.665 percent and the 30-year breaking out to multi-year highs. The cross-asset signal that mattered most was not in equities at all. Silver fell 3.81 percent on the session, the deepest red in the metals complex, which historically accompanies commodity-currency stress and a broader institutional flight from risk-weighted positioning.

The question Wednesday answers is not what the market will do tomorrow. It is which of two narratives wins. Either the dispersion structure that institutions have built over the past two months holds together through one more catalyst stack, or the rate breakout finally pulls the rug on the AI mega-cap concentration that has driven the entire year-to-date rally.

How the desk is positioned into the binary

A pattern emerged Tuesday that institutional desks are reading carefully. Fixed-strike implied volatility declined approximately half a vol point across the curve during the session, even as the index sold off three quarters of a percent. The standard reading is that when spot falls and volatility falls with it, hedging demand has been muted. Either traders are already long protection from prior weeks and have no incremental need to add, or traders genuinely do not believe Nvidia will produce a sharp downside reaction. The bullish interpretation says positioning is too clean to provide ammunition for a real flush. The bearish interpretation says the absence of hedges is itself the risk. If the Nvidia print disappoints, the lack of pre-existing protection means a sharper-than-expected sell move once positioning unwinds Thursday.

What can be measured directly is the dispersion. Session data Tuesday showed heavy institutional call selling at SPY 735 and 736, the same strike zone where ARM call writers had been active earlier in the week, plus QQQ 705 and 706. Institutions are writing upside calls at these strikes because they view SPX 7,400 as the structural cap into Wednesday's catalyst stack. At the same time, the single-name long-dated bullishness has not retreated. The largest single trade on Tuesday's session was 4,300 contracts of Nvidia partner Nebius January 2027 calls at $66.25 each, approximately $28.5 million in premium, on a name Nvidia recently invested $2 billion in directly. ARM August $170 calls printed 5,000 contracts at $59.95, $30 million in premium, executed at the offer.

The institutional read is clean. Bullish AI single-name into 2027. Bearish the index into Wednesday's close.

The architecture of Wednesday

The expected range for the session is SPX 7,317 to 7,410, derived from the options-implied 0.63 percent one-day move and confirmed by the 14-day ATR-based projection of 7,275 to 7,433. Inside that envelope, the structural pivots that matter are concentrated tightly.

Above the Tuesday close, three levels gate any upside reclaim. The Tuesday Y-VAL at 7,375 SPX (approximately ES 7,397) marks the lower edge of Tuesday's value area and the 20-day moving average confluence. A move back above with a four-hour close confirms a mean-reversion bounce. The 7,388 first pivot resistance and the 7,395 volatility inflection level sit immediately above and align with the heavy call-writing zone. Through 7,400, the next high-probability combo strikes are 7,403 at 93.30 percent and 7,410 at 84.04 percent. Above 7,410, the air thins quickly until 7,425 to 7,440, the prior session's intraday rejection zone.

Below the Tuesday close, the structure tells a tighter story. The 7,329 combo strike prints at 92.57 percent probability and aligns with the 0DTE put support at 7,330. The 7,322 level is the Fibonacci 38.2 percent retracement of the April 27 to May 14 rally and the highest-probability deeper target. Below 7,310, the customer negative-gamma zone opens up and dealer hedging flips from suppressive to amplifying. Through 7,300, the third pivot support and the round number act as the line where chart-based stops convert into liquidity grabs.

The 20-day moving average at 7,375 is the structural test. Closing below it for a third consecutive session confirms the daily momentum break. Reclaiming and closing above it before Fed Minutes invalidates the bear thesis from the prior three days and points the index back toward the call-writing wall at 7,400.

What the Fed Minutes does

The market is pricing meaningful hawkish risk into the 2:00 PM release. The yield breakout backdrop forces the question. The 2-year is above 4 percent for the first time in a year. The 30-year is at multi-year highs. The 20-year Treasury auction at 1:00 PM ET, one hour ahead of the Minutes, is itself the test of foreign demand for duration paper. Reports earlier in the week pointed to Chinese and other foreign holders reducing USD bond exposure incrementally, and a soft auction would accelerate the bear-steepener heading into the Minutes release.

The Minutes themselves do not contain new policy. They re-anchor interpretation of the prior meeting. The realized volatility they produce depends entirely on whether the prior committee discussion reads as more concerned about inflation persistence or more concerned about labor-market softness. The hawkish path pushes the 10-year toward 4.75 percent, accelerates the equity selloff, and drives SPX toward the 7,329 put wall and the 7,322 Fib. The dovish path eases yields, lifts equities back to the 7,395 volatility inflection level, and possibly higher. The base case, given the rate backdrop, leans hawkish. The probabilities are not symmetrical given where positioning sits, but neither is the path predictable on the data side.

What Nvidia does

The implied move on Nvidia for Wednesday's after-hours print is approximately 6 percent. That is, in dollar terms, a move from 220 to either 233 or 207. In percentage terms, that translates to roughly 50 to 100 ES points of gap risk in either direction at Thursday's open. The earnings call is at approximately 4:20 PM ET, twenty minutes after the cash session closes.

The trade for Wednesday is not to position into the print. It is to recognize that Wednesday's close is a setup for Thursday's gap, not a destination in itself. The institutional positioning bias going in is dispersed long single-name AI, short index, and that structure is not going to be unwound by any one print. What changes Thursday is the gap direction.

A positive print, with revenue beating consensus and Q2 guidance above the bar, gaps ES up 50 to 100 points overnight and brings 7,425 to 7,447 into play as the structural target. The 7,447 combo strike sits at 98.83 percent probability and is the highest-probability ceiling in the entire Wednesday matrix. A negative print, with any guidance miss or AI capex concern, gaps ES down through 7,310 into the negative-gamma amplification zone. The downside scenario, once below 7,304 dealer gamma flip, opens 7,280 to 7,295 as the Thursday-open target.

The trade for Wednesday

The primary setup is mechanical. Short fade the 7,375 to 7,395 Y-VAL retest from below if and when price returns to that zone, with stop above the 7,393 Pivot 1st Resistance. First target is the 7,343 Pivot 1st Support. Second target is 7,330, the put wall plus 92.57 percent combo confluence. Third runner is 7,313, the dealer gamma flip area. The risk-reward at target one is approximately 1 to 1.7. At target two it is 1 to 2.7. At target three it is 1 to 3.5. Position size is half normal or less, given the binary that follows.

The secondary setup is a breakdown trigger. A confirmed 15-minute close below SPX 7,329 with negative tick activates the institutional stop concentration and the dealer amplification mode. Entry on the close confirmation in the 7,355 to 7,360 ES zone. Stop above 7,378 ES at the Tuesday close reclaim. Target 1 at 7,335 ES, target 2 at 7,322 ES, runner 7,300 ES into the customer negative-gamma zone. The trigger for this setup is most likely a hawkish Fed Minutes.

No swing positions are carried through the 4:00 PM close. The Nvidia print is binary and 6 percent is a wide tail in either direction. The institutional play is to be flat into the print and react to Thursday's open with full directional information.

The cross-asset signal

Two cross-asset patterns matter into Wednesday. The first is silver. Silver fell 3.81 percent Tuesday, by a wide margin the deepest red in the metals complex. Heavy silver selling historically accompanies major risk-off rotations because silver carries the highest beta to global liquidity contractions among precious metals. Tuesday's silver print is consistent with a broader institutional rotation away from risk-weighted positioning ahead of the catalyst stack.

The second is the VVIX. The volatility-of-volatility index rose 3.76 percent to 95 Tuesday. The VIX itself was modestly higher at 18, suggesting subdued realized fear. The divergence between rising VVIX and contained VIX is the technical signal that institutions are starting to build positioning for the catalyst rather than buying outright protection. Tomorrow may produce the volatility expansion that VVIX is signaling.

The Wednesday read

The bias is range-bound bearish into 2:00 PM Fed Minutes, with the 20-day moving average at 7,375 as the structural test. Tactical setups only. Half size or less. No swing trades through the close. The largest opportunity of the week is Thursday on the post-Nvidia reaction, not Wednesday before the print. The job tomorrow is patience and execution on tactical fades; the job Thursday is to read the gap and trade direction. Confusing the two is the way the day gets lost.

Foundational guides

New to S&P 500 futures? Start with What Are ES Futures, the ES, NQ, MES & MNQ point value and contract specs, gamma exposure (GEX) explained, and market internals: TICK, ADD, VOLD and VIX.