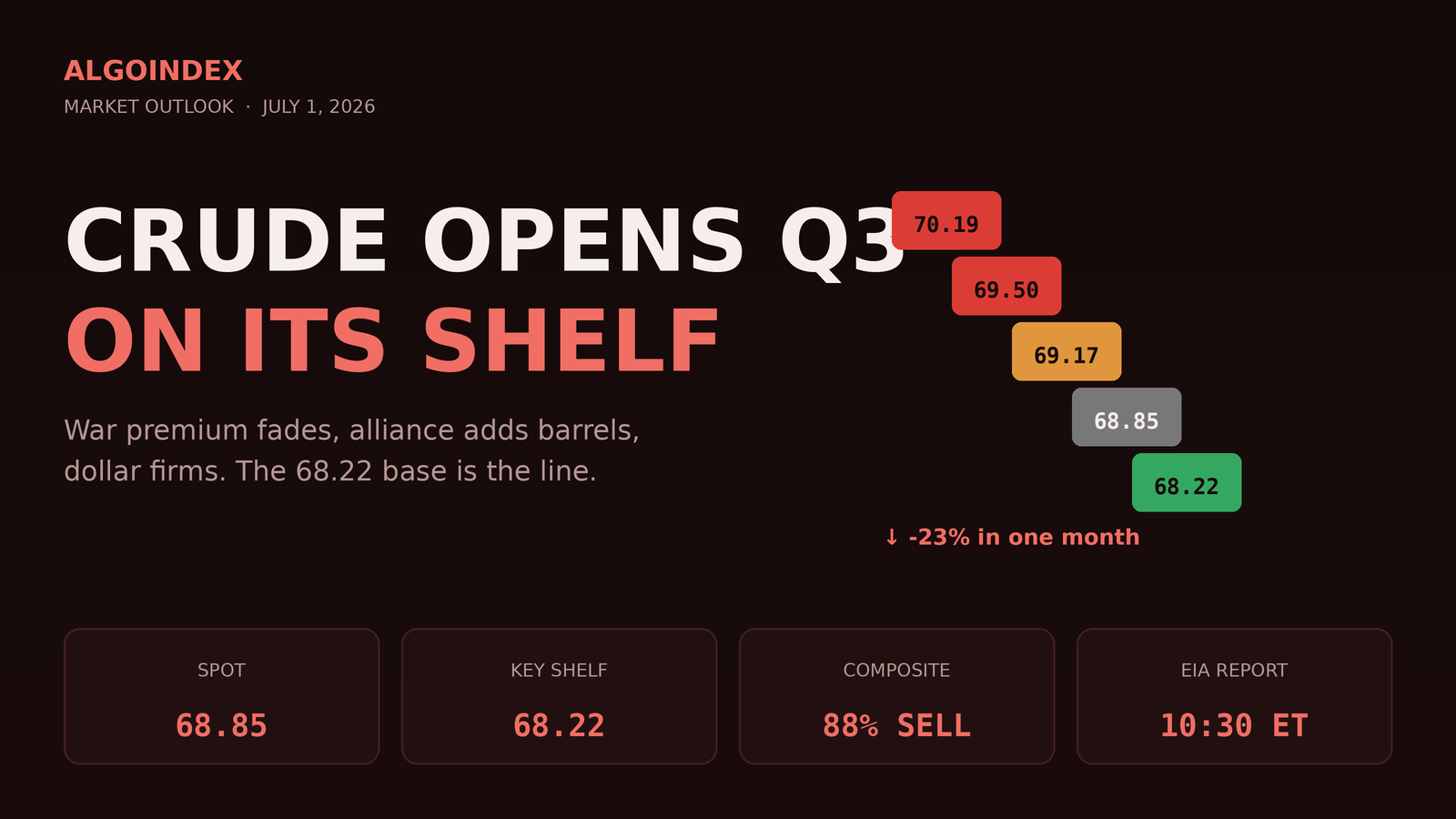

West Texas Intermediate opens the new month on the back foot, trading near 68.85 in early activity, down roughly 0.8 to 0.9 percent from the prior settle of 69.50. The contract spent the overnight session grinding along its lows, printing a range of 68.22 to 70.19 and sitting in the lower third of that band as the cash open approaches. The dominant driver is the unwind of the geopolitical risk premium that had been priced into crude through late June: reports of progress in talks between the United States and Iran have removed a large part of the Strait of Hormuz war premium that spiked the complex in the final week of the month, and the newswires frame it plainly as oil falling further after peace talks.

Two more headwinds sit on top of the fading war premium. Producers in the extended alliance are reported likely to raise August output quotas by roughly 188,000 barrels per day at their weekend meeting, extending a run of managed increases that signals a group prioritizing market share over price. A firmer dollar, with the dollar index up about 0.25 percent near 101.43, makes dollar-denominated crude more expensive for overseas buyers. Together, a fading war premium, an expected supply increase, and dollar strength have driven a punishing one-month decline of nearly 23 percent in the front contract. The contradiction into today is that price is now stretched into a well-defined support base, and the single most important event of the session, the 10:30 ET government inventory report, sits directly above it.

Three forces, all pointing down

The supply narrative turned bearish overnight. The extended producer alliance is likely to lift August quotas by about 188,000 barrels per day at its weekend meeting, and offsetting that only at the margin is a flagged fuel-supply disruption tied to logistics issues at some producing-nation refineries, a supportive but secondary factor. Demand signals are soft: the morning private-payroll estimate came in weak at 98,000 against a 120,000 expectation, feeding a broader read of cooling United States activity that weighs on forward fuel demand, with the mid-morning manufacturing surveys set to sharpen the picture. Global growth concerns, thin refining margins, and uncertain Chinese buying leave the complex without a compelling consumption story to lean on.

Geopolitics is the swing factor and it has flipped from tailwind to headwind. The late-June spike was driven by military activity around the Strait of Hormuz and reported strikes on shipping; the current session is pricing the opposite as progress in United States and Iran talks unwinds the war premium. A residual risk remains, with a fresh maritime-security report of an incident roughly 85 nautical miles off the Yemeni coast a reminder that shipping-lane risk has not vanished. The dollar adds the third headwind, firm near 101.43 as markets await commentary from the Federal Reserve chair and weigh a less-dovish path. A firmer dollar mechanically pressures dollar-priced crude, and with a full slate of central-bank speakers on the calendar, the rate-and-dollar linkage is an active driver rather than background noise.

The structure, level by level

Immediate overhead sits at the 68.91 to 69.17 band, a shelf of intraday micro-pivots that also captures the computed target at 69.17 and the session lower high near 69.13. Above that, 69.50 is the prior settle and the first meaningful line a bounce must reclaim to shift the intraday tone, with the 70.11 daily pivot and 70.19 session high forming the next paired ceiling. A push through there exposes the 70.74 one-standard-deviation resistance and the 70.99 first pivot resistance, then the stretched objectives at 71.26, 71.66, the 72.23 extension, and the 72.49 second pivot resistance, with 73.37 marking the outer edge of any relief rally.

Underneath, immediate support is the 68.61 first pivot support, backed almost immediately by the 68.26 one-standard-deviation support and the 68.22 session low, which doubles as the one-month and 13-week low. That confluence at 68.2 to 68.6 is the pivotal support base for the session. A decisive break opens the 67.74 and 67.73 pairing, then the 67.34 three-standard-deviation support and the 66.78 average-cross shelf, with the 66.23 third pivot support the extended objective before the June lows, the 65.70 extension, and the far 55.39 52-week low. Every meaningful moving average sits overhead and slopes down, from the 9-day cross near 71.83 up to the 40-day near 85.64, so rallies sell into supply until at least the low-70s is reclaimed.

The complete data picture

Level map (CL futures)

| Zone | Level (CL) | What it is |

|---|---|---|

| Resistance | 73.37 / 72.49 | 3rd / 2nd pivot resistance (outer relief) |

| Resistance | 71.66 / 71.26 / 72.23 | 3rd, 2nd s.d. band and upside extension |

| Resistance | 70.99 / 70.74 | Pivot R1 / 1st standard-deviation band |

| Resistance | 70.11 / 70.19 | Daily pivot / overnight high |

| Resistance | 69.50 | Prior settle (first reclaim line) |

| Shelf | 68.91 to 69.17 | Micro-pivots + computed target 69.17 |

| At market | 68.85 | Spot, lower third of the overnight range |

| Support | 68.22 to 68.61 | Pivot S1 68.61, 1 s.d. 68.26, low 68.22 (key base) |

| Support | 67.74 / 67.73 / 67.34 | 2 s.d. / 2nd pivot / 3 s.d. support |

| Support | 66.78 / 66.23 / 65.70 | Cross shelf / 3rd pivot / extension |

By the numbers

Standard-deviation bands off the 70.11 pivot: 1 s.d. 68.26 to 70.74, 2 s.d. 67.74 to 71.26, 3 s.d. 67.34 to 71.66. Moving-average cross levels: 9-day 71.83 (stall 76.01), 18-day 78.06, 40-day 85.64, all overhead and sloping down. Composite 88% sell, with 20-day and 50-day both at 100% sell. Cross-asset: Dollar Index near 101.43 (+0.25%), gold near 4,042, equity vol gauge 16.7 (+1.2%), broad-index futures about -0.15%, tech-heavy futures about -0.45%. Private-payrolls preview 98,000 versus 120,000 expected. No listed-options dealer-positioning surface exists for crude; the lens here is the energy-complex and term-structure read, with front-end weakness relative to deferred months consistent with spot risk repricing lower as the war premium fades.

The three paths (desk probabilities)

Path A, bearish (about 45%): price loses 68.22 after the inventory data and works toward 67.74, then 67.34.

Path B, range (about 35%): the shelf holds and price chops 68.2 to 69.2 all session as the crowded short and the oversold reading offset the down-trend.

Path C, relief bounce (about 20%): a supportive draw plus short-covering reclaims 69.50 and challenges the 70.11 pivot toward 70.74.

Expected range today: low scenario 67.74 to 67.34 extending to 66.78 on a bearish inventory surprise, most-likely containment 67.7 to 70.1 oscillating around the 68.2 to 69.2 band, high scenario a reclaim of 69.50 pressing 70.11 toward 70.74.

Today's calendar (ET)

- 09:00 · Central-bank governors speak (United States, euro area, Canada, United Kingdom)

- 09:45 · US final manufacturing survey, near 55.7

- 10:00 · US manufacturing index, prices paid, employment, construction spending, plus euro-area central-bank president remarks

- 10:30 · Government crude-oil inventory report (forecast draw about 2.3 million barrels, prior draw about 6.1 million) · first-order catalyst for crude

- 13:00 and 15:00 · US official events and remarks

- Following morning · Monthly employment report and weekly jobless claims (payrolls pulled forward ahead of the July 4 holiday)

The setup respects the trend while honoring the catalyst. The higher-conviction posture is a with-trend short on a bounce into the 68.90 to 69.20 shelf and the computed 69.17 target, ideally on a rejection candle, targeting the 68.22 base, then 67.73, with 66.78 to 66.23 the extended objective and a stop at 69.60 above the prior settle. A secondary with-trend entry is a break-and-retest short below 68.22 once the inventory report confirms weakness. The management rule is firm: stand aside through the 10:15 to 10:45 ET window and trade the resolution of the print, not the anticipation.

The mirror is a half-size, quick-management relief long only on a clean reclaim of 69.50 then the 70.11 pivot with a supportive draw behind it, targeting 70.74 then 71.26 with a stop back below 69.50. That is a counter-trend idea against a market carrying an 88 percent sell composite and a fresh supply headwind, so it earns a smaller size and a tighter leash. Crude rests one rung above its shelf this morning, a heavily short market pressed into major support with a scheduled inventory print directly overhead. Today the barrel trades the draw, not the story.

Trade the levels, not the noise.

AlgoIndex marks the key session levels before each open and scores whether they hold. See the running numbers in the gamma level accuracy tracker, then view pricing.

Foundational guides: gamma exposure explained, call walls and put walls, and market internals.