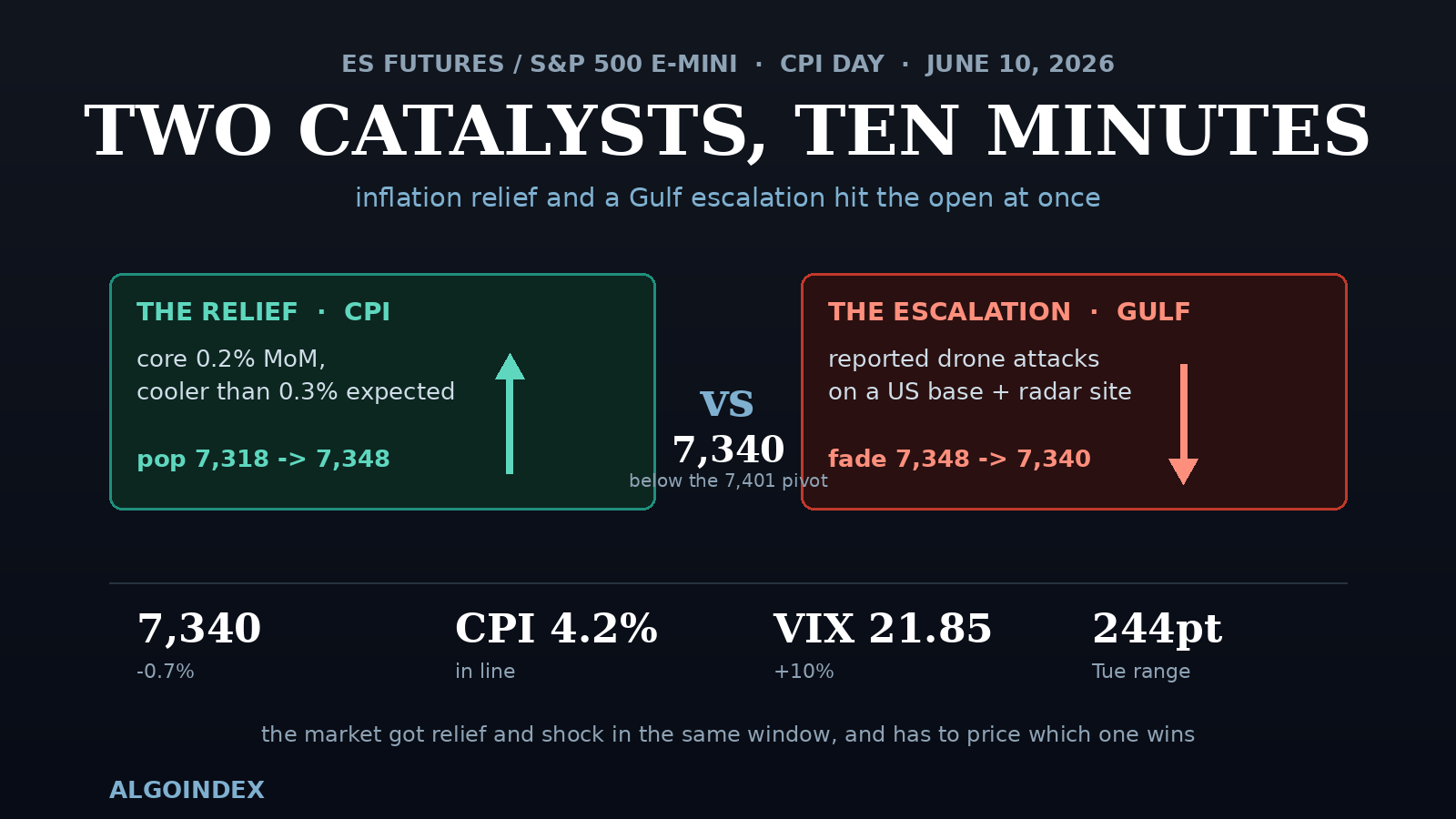

For a week the market waited on one number. When it finally arrived this morning, it brought company. At 8:30 ET the May consumer-price report landed almost exactly on consensus, the inflation relief the equity bid had been hoping for. But minutes earlier, wire reports described drone attacks on a US air base and a radar site in the Gulf, and the geopolitical escalation the market had been fading for weeks suddenly looked real. The S&P 500 E-mini got its relief and its shock inside the same ten minutes, and now has to price which one wins. It enters Wednesday's cash session near 7,340, down about 0.7 percent from Tuesday's settle, sitting below the dealer pivot that turns the whole session bearish, in the part of the level map where hedging amplifies rather than absorbs.

Two Catalysts, Ten Minutes

The clean way to read the open is as a collision. On one side, the inflation print delivered relief: headline came in at 4.2 percent year-over-year, exactly consensus and the first 4-handle since 2023, but the mechanical driver is the energy shock plus a low year-ago base, not a broad reacceleration, and core actually undershot at 0.2 percent on the month against a 0.3 percent expectation. That cooler core detail produced an immediate pop from 7,318 to 7,348. On the other side, the geopolitical headline reasserted within minutes: the reported drone attacks on a US base and radar site in the Gulf, layered on a sharp escalation in rhetoric on Iran, dragged price back toward 7,340. The market got both inputs in the same window, and the session is now a fight over which one dominates.

Tuesday Set the Stage: A 244-Point Round Trip

To understand today's fragility, look at yesterday's session, a structural earthquake disguised as a quiet close. The contract opened at 7,458.50, tagged 7,491 in the first hour, then broke the 7,390 cash pivot late morning and cascaded roughly 200 basis points lower to a 7,247.25 low by midday, before spending the entire afternoon recovering to settle within a point of the very pivot it had broken. Real-time hedging flow reached roughly minus 7 billion dollars of cumulative single-stock delta at the lows before reversing near 12:30 PM, and same-day positive gamma concentrated near the 7,215 strike provided the support the recovery launched from. A market that probes both extremes and closes undecided is a market storing energy, and the overnight session spent that energy lower.

Why the Pivot Is Everything Today

The single most important number on the board is the 7,401 dealer pivot, roughly 7,390 in cash terms. It is the line the institutional desk has drawn between bearish-below and constructive-above, and it sits just under the dealer gamma flip at 7,410. The market opened below both, which puts it in amplification mode: in this zone, dealer hedging runs with the move and extends it rather than cushioning it, and the desk has stated it stays out of equities until the pivot is reclaimed. That is the structural reason the burden of proof sits with the bulls. Reclaim 7,410 with healthy internals and the bias flips two-way toward the 7,431 volatility inflection; fail at the pivot and the put-heavy surface points down toward the 7,311 support shelf, where bearish positioning is thickest and a responsive bounce is most likely on first touch.

What the Inflation Print Actually Said

The headline 4-handle looks alarming until its composition is read. Institutional previews had framed anything at or under roughly 4.2 percent as the relief case and anything above 4.3 percent as the print that would force the front end to price further tightening. The number printed exactly at the relief line, and the cooler core, 0.2 percent on the month, undershot. The dollar is flat near 99.97 and the overnight financing rate eased. But the relief has to survive a heavy rate stack: a 10-year auction this afternoon, producer prices tomorrow with a consensus already pegged at a multi-year-high 6.4 percent year-over-year, a European rate hike expected tomorrow morning, and the home policy decision next Wednesday with fresh projections. Today's relief on core is one clean reading inside a week that keeps testing it.

The Tech Pressure Point and the Gold Anomaly

Two cross-currents define the market underneath the headline. First, technology remains the pressure point: the Nasdaq-100 future is down 1.4 percent and underperforming the broad index for a second straight session, with Tuesday's session showing explicit rotation out of the artificial-intelligence complex into financials, healthcare and consumer discretionary. The single most important corporate read of the week, a major database company's results, lands after tonight's close as a direct gauge of AI capital spending, while the same trade is being de-risked. Second, the gold anomaly: the metal liquidated almost 3 percent on a risk-off morning, the opposite of how a safe haven should behave when war headlines cross. That is the fingerprint of forced de-grossing or margin-driven selling, and the combination of falling gold, rising oil, and rising equity volatility is an unusual, unstable mix that historically resolves with a violent directional equity move rather than a quiet one.

Four Ways the Session Resolves

With two live catalysts pulling in opposite directions and a thin, decaying dealer cushion, the distribution of outcomes is genuinely four-sided. The afternoon's scheduled risk is a 10-year auction at 1:00 PM; the unscheduled risk is the next Gulf headline.

The Setup: Sell the Relief Into the Pivot

The dealer surface amplifies moves below the 7,401 pivot, institutional desks are explicitly out of equities below it, and broad flow is put-heavy into a catalyst stack that runs through tonight and tomorrow. That makes a post-CPI relief rally into the 7,388 to 7,402 confluence, where the prior settle, the overnight high, the value-area high and the dealer pivot all stack inside 14 points, the day's best-defined supply to lean against.

Yesterday the market coiled inside a box, waiting on a number. Today the number arrived clean, and a second catalyst arrived with it. The inflation relief is real but shallow, the escalation is real but unconfirmed, and the dealer surface sits in the part of the map where moves get amplified rather than absorbed. Until the 7,401 pivot is back overhead, the burden of proof stays with the bulls, and with a database giant reporting tonight, producer prices and a European rate decision tomorrow, and the home policy meeting next week, the catalyst stack does not thin out, it thickens. Trade the pivot, watch the crude market for the escalation read, and respect that a thin afternoon cushion means whichever way this breaks, it can run.

This analysis is for educational purposes and reflects conditions around the Wednesday, June 10, 2026 cash open, a fast-moving session with live geopolitical headlines. It is not investment advice. Markets carry risk; conduct independent research before acting.

Foundational guides

New to S&P 500 futures? Start with What Are ES Futures, the ES, NQ, MES & MNQ point value and contract specs, gamma exposure (GEX) explained, and market internals: TICK, ADD, VOLD and VIX.