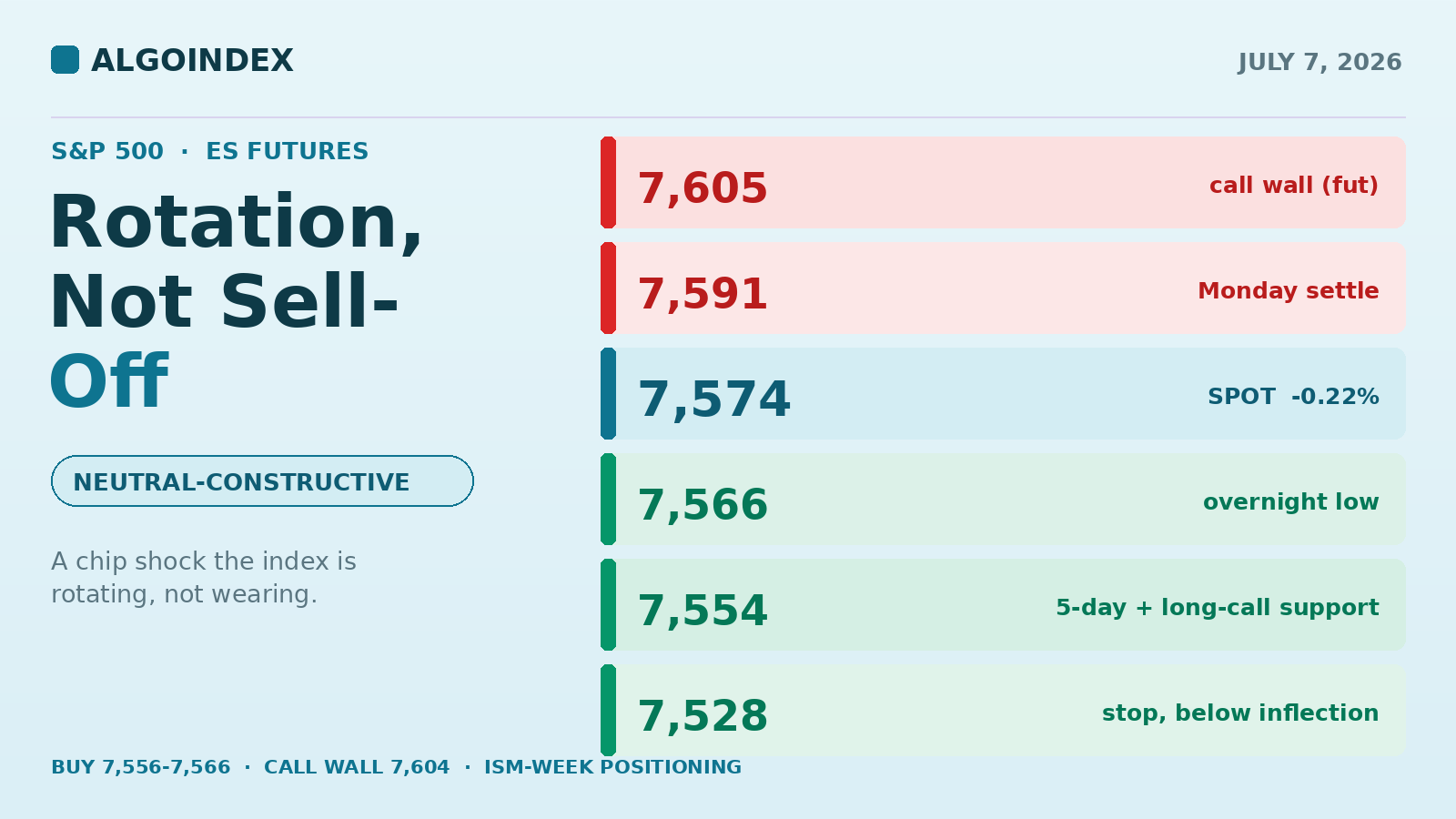

ES opens Tuesday at 7,574, down just 0.22 percent, while Nasdaq futures are off more than 1 percent and Dow futures are green. That spread is the whole story: an Asian semiconductor unwind is being rotated, not liquidated, into software, platforms, and financials. Dealer positioning stays supportive above the 7,530 inflection with heavy long-call support at the 7,554 zone. The plan: buy the 7,556 to 7,566 demand stack toward 7,590 and the 7,604 call wall, and stand aside if 7,529 breaks. Bias neutral-to-constructive, conviction moderate.

Between the moment Samsung reported a 19-fold jump in profit and the moment its stock fell 10 percent in Seoul, the entire complexion of the week changed. The Kospi dropped 8 percent and tripped a trading halt, memory names bled worldwide, and Nasdaq futures gapped lower. ES gave up only 17 points. That gap, a full percent of daylight between the Nasdaq and the S&P, is the number that matters this morning.

Money is moving, not leaving. Microsoft rose 1.5 percent in early European trade, Amazon and Alphabet caught rotation bids, and Dow futures printed green while chips sold off, the clean signature of a sector rotation rather than a broad de-risking. In yesterday's note we flagged 7,607 as the top of the dealer-resistance stack; Monday's rally ran into the call wall at that 7,605 equivalent and stalled almost to the tick. Today the market defends the other side of that structure, the long-call support zone just under 7,566, with tomorrow's FOMC minutes already pulling on the session.

Rotation, not liquidation

Monday's RTH session was one-way constructive. The cash index rose 0.72 percent to a 2.5-week high at 7,537, the Nasdaq-100 gained 1.26 percent, semiconductors rallied over 2 percent, and the Dow printed a fresh all-time high. The September E-mini settled 7,591.50. Overnight, price opened 7,597, tagged 7,601.25 in early evening, then sold progressively as Asia absorbed the Samsung print, bottoming 7,563.00 before recovering to 7,574, a 38-point range on roughly 130,000 contracts with open interest near 1.95 million.

The daily trend stays intact. ES has run nearly 13 percent off the late-March low at 6,401.75 and sits about 1.5 percent under the June 2 contract high at 7,693.75. The last month has been a wide consolidation: the June 11 pullback low at 7,292.25 held well above prior breakout structure, and the one-month high at 7,648.75 from June 15 is still unchallenged. Price sits in the upper quarter of that range and above the 20-day at 7,501, with a five-day change of plus 76.75 points. This week's dip is a shallow give-back inside a rising channel. The rally off the June 26 swing low near 7,360 remains a clean sequence of higher highs and higher lows into the 7,601.25 overnight peak; the overnight sell-off printed the first meaningful lower high on the 15-minute frame, but the higher-timeframe swing holds as long as 7,563 does.

The moving-average stack is fully bullish and untested: the 5-day (7,557.70), 20-day (7,501.23), 50-day (7,485.66), 100-day (7,182.54), and 200-day (7,081.67) sit below spot in perfect ascending order. Price trades 16 points above the 5-day and 73 above the 20-day. The 5-day sits inside today's primary demand zone; the 20-day and 50-day converge in the 7,485 to 7,501 band, the deeper target if the week turns risk-off. Momentum is elevated but not extreme, the 14-day relative strength at 55.88 is mid-range, though the 9-day raw stochastic at 89.6 percent and the 100-day stochastic above 90 percent flag short-term overbought after five up sessions in six. The directional index reads 19.08 with the down-line (18.70) fractionally above the up-line (15.67), the signature of a strong market pausing rather than turning. The composite reads 56 percent buy and strengthening, short-term systems 40 percent, medium-term 75, long-term 67.

A market where breadth holds while chips bleed is a consolidation, not a top.

The dealer support under the dip

Dealer positioning on the cash index stays in a stabilizing posture. Monday closed 7,537, above the volatility inflection level at 7,475 (roughly 7,530 in futures terms), keeping dealers in positive gamma where they sell strength and buy weakness. The call wall stands at 7,550 cash, about 7,605 in futures terms, directly above Monday's close, and it capped the session. The put wall sits at 7,300 cash, near 7,354 futures, with the major open-interest magnet far below at the 7,000 cash strike. Critically, the 7,500 cash strike carries roughly 50,000 dealer long calls and acted as support all of Monday; it translates to about 7,554 on the futures board and anchors today's primary demand zone.

Monday's flow was decisively bullish. Real-time hedging-flow data recorded about plus 5 billion dollars of delta notional in single stocks, the highest of the past 30 days, driven by longer-dated call buying, plus 1.9 billion on the index side driven by same-day call buying. Against that, the desk commentary has turned tactically cautious, adding put positions since July 1 and framing the bigger opportunity as a multi-week correction from bullish-positioning extremes, while still allowing for a push toward 7,550 to 7,600 cash first. The volatility surface carries the tell: one-month implied volatility at 12.5 percent trades well below one-month realized near 17.7 percent, the implied-volatility rank is a low 14 percent, and the implied one-day move is about 59 cash points. Yet the skew rank near 92 percent shows tail protection is being bid even as headline volatility sleeps. Puts outpaced calls overnight, roughly 783,000 to 547,000, with a put-call open-interest ratio of 1.26.

"A supportive positive-gamma environment today, with hedging demand underneath. The market is one catalyst away from a faster repricing if the 7,530 futures inflection fails."

Positioning across the board is crowded long and increasingly hedged. Commitment-of-traders data through June 30 shows leveraged funds cut their short book by 47,501 contracts on the week while asset managers trimmed longs by 22,692, so the short-covering tailwind is largely spent. That does not break the trend by itself, but it removes a layer of fuel and makes the market more sensitive to negative catalysts, exactly like the overnight chip news.

Yields firm, and a tanker gets hit

The rates backdrop turned incrementally hostile overnight. The dollar index is flat near 100.91 while Treasuries weakened, the 10-year yield rising 2 basis points to 4.49 percent as money markets nudged toward tighter-policy pricing, a notable move given last Thursday's payrolls shock of 57,000 against a 113,000 forecast. Fed Governor Bowman spoke at 7:00 ET and offered no policy content. The real event risk is tomorrow's FOMC minutes at 2:00 PM ET, with today's 1:00 PM ET 3-year note auction (prior high yield 4.192 percent) the cleanest interim rates catalyst. Equity risk today is the interaction between rising yields and stretched tech valuations.

Leadership is rotating violently within technology. Monday's advance was chip-led with semiconductors up over 2 percent; overnight, Samsung's disappointing-despite-excellent print took the sector down globally, and Micron and Sandisk fell more than 5 percent in premarket. Microsoft, Amazon, and Alphabet caught rotation bids in Europe. A newly public rocket-and-satellite company joins the Nasdaq-100 before today's open, which should generate passive index buying in that name. Bank earnings begin July 14, and options positioning shows investors building bullish exposure in financials ahead of the season. The geopolitical picture is live again: a laden LNG carrier was struck by a projectile near the Omani coast overnight despite the late-June peace agreement, lifting Brent 0.9 percent to 72.66, and the NATO summit convenes in Ankara with the US president attending. Cross-asset stress is quiet, the VIX at 15.95 is up 2.5 percent but within a hand of three-month lows, gold trades lower near 4,156, and the yen sits near 161.8 with hedge-fund positioning the most bearish since 2007 even as Japan's 30-year auction drew the strongest demand since 2019.

The trade: buy the long-call shelf

The 7,554 to 7,566 band stacks the overnight low, the 5-day average, two-standard-deviation support, and the dealer long-call strike into one defended zone. Buy tests of 7,556 to 7,566 after 09:45 ET with stabilizing internals. Stop 7,528, below the 7,530 volatility inflection and the 40-day crossing point, because a trade there means the hedging environment flipped from stabilizing to amplifying. Targets 7,590 (Monday settle reclaim), then 7,604 (overnight high and call wall confluence), then 7,621 (first pivot resistance). From a 7,561 blended entry on 33-point risk that is roughly 1:0.9, 1:1.3, and 1:1.8. Invalidation is a 30-minute close below 7,542, or entry-zone failure on expanding volume with the ES-NQ spread widening.

The alternate is a fade at defended supply: short on rejection at 7,600 to 7,605, the overnight high plus call-wall plus computed-target confluence, if the first test arrives with weak breadth and Nasdaq underperformance persisting. Entry 7,598 to 7,604, stop 7,616 above one-standard-deviation resistance, targets 7,585 then 7,566. In a positive-gamma environment, take profits quickly and do not press through the settle reclaim. Skip everything if price chops between 7,566 and 7,585 with mixed internals, if the opening 15 minutes fully tests both 7,563 and 7,585, or if a headline shock hits the entry window.

Today's economic calendar (ET). Light on first-order US prints; the session trades the chip reset and rotation.

Base-case distribution for the RTH session. Path C carries the VIX back through 17.

Dips get bought while the dealer environment stays positive. Upside beyond the call wall needs fresh fuel that the chip complex is not offering today.

The complete data picture

Every level and reading from the morning ES review, top to bottom. Nothing rounded away.

| Resistance (top to bottom) | Support (top to bottom) |

|---|---|

| 7,693.75 to 7,700.17 52-week high, third pivot resistance | 7,563 to 7,566 overnight low, one-SD 7,565.65 (cash ~7,510) |

| 7,648.75 to 7,659 one-month high, second pivot 7,651.33, low-vol inflection (7,605 cash) | 7,554 to 7,558 5-day MA 7,557.70, two-SD 7,554.94, 7,500-cash strike (~50k long calls) |

| 7,628 to 7,636 two- and three-SD extensions | 7,542.67 to 7,546.72 first pivot support, three-SD |

| 7,617.35 one-SD; 7,621.42 first pivot resistance | 7,529 to 7,530 volatility inflection (fut), 40-day MA cross (character line) |

| 7,601.25 to 7,605 overnight high, target 7,604.83, call wall (7,550 cash) | 7,494 to 7,501 second pivot, 20-day MA, 50% momentum midpoint |

| 7,585 to 7,591.50 9/18-day MA cross 7,585.75, Monday settle | 7,464 third pivot; 7,434 dealer pivot (7,380 cash); 7,354 put wall (7,300 cash); 7,292.25 one-month low |

Moving averages: 5-day 7,557.70, 20-day 7,501.23, 50-day 7,485.66, 100-day 7,182.54, 200-day 7,081.67. Performance: 3-month about +13%, five-day +76.75 (+1.02%), about 1.5% below the June 2 high 7,693.75. Dealer map (cash / fut): vol inflection 7,475 (~7,530 fut), call wall 7,550 (~7,605), put wall 7,300 (~7,354), magnet 7,000; 7,500 strike ~50k dealer long calls (~7,554 fut).

Intraday prints: overnight open 7,597, high 7,601.25, low 7,563.00, near 7,574, 38-point range, volume ~130K, open interest ~1.95M. Monday cash +0.72% to 7,537 (2.5-week high), Nasdaq-100 +1.26%, Dow all-time high. Expected range: low 7,530 to 7,545, mid 7,555 to 7,600, high 7,610 to 7,625; implied-move envelope 7,543 to 7,640; one-ATR outer 7,493 to 7,690. Paths: A 55% (hold 7,554 to 7,566, recover 7,590 to 7,605); B 30% (break 7,563 to 7,542 to 7,530, inflection holds, close 7,560 to 7,575); C 15% (7,529 fails, trend to 7,494 to 7,500, VIX >17). Setup: long 7,556 to 7,566, stop 7,528, T1 7,590, T2 7,604, T3 7,621, R:R 1:0.9 / 1:1.3 / 1:1.8. Alternate: short rejection 7,598 to 7,604, stop 7,616, targets 7,585 then 7,566. Macro override: fresh Hormuz escalation, a hard auction failure, or Kospi-style chip contagion suspends the setup. Calendar (ET): 8:30 US + Canada trade balance; 10:00 Canada Ivey PMI; 11:00 NY Fed inflation expectations; 12:00 EIA short-term energy outlook (tentative); 1:00 US 3-year note auction (prior 4.192%); 10:00 PM RBNZ (2.5% expected); Wednesday 2:00 PM FOMC minutes.

A chip shock the S&P is rotating, not wearing.

See how AlgoIndex turns this kind of read into systematic signals. Read today's Nasdaq note and the pillar on how dealer call and put walls behave.

View pricing