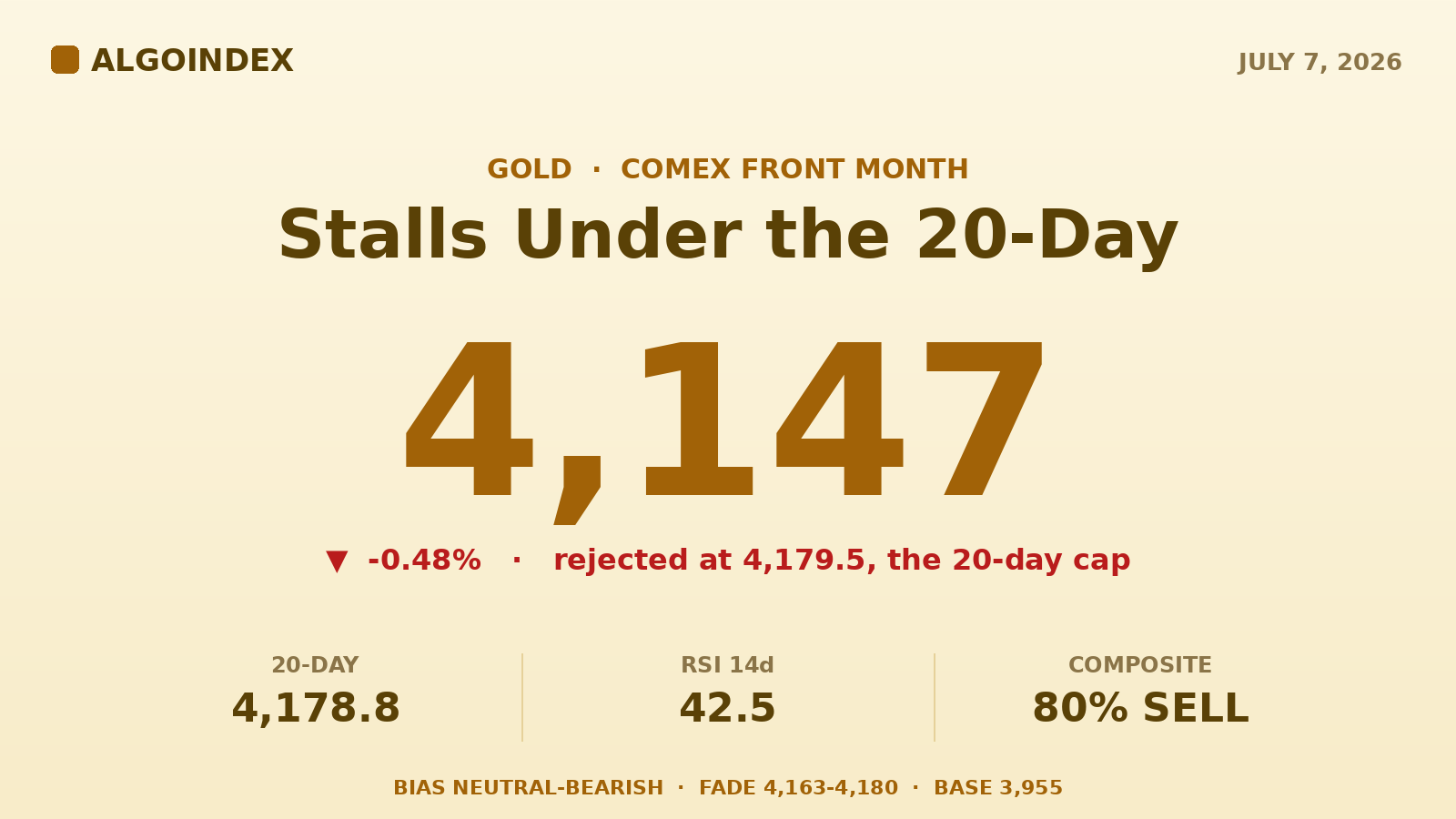

Gold pushed to 4,179.5 overnight, stalled to the tick under its 20-day average, then swept down to 4,127.7 before recovering into the mid-4,140s, off 0.48 percent near 4,147. A five-day, 110-point bounce off the June base has run into a wall: every medium and long-term trend measure still points down, the composite reads 80 percent sell, and dealer positioning amplifies moves in both directions. The plan: fade strength into the 4,163 to 4,180 supply band toward 4,129 and 4,115, stop above 4,192. Bias neutral-to-bearish, conviction moderate, the burden on buyers to reclaim 4,172 and hold it.

Three points. That is all the overnight rally could add before it broke. Gold opened the Globex session at 4,176.4, managed 4,179.5, and then rolled over through Monday's entire afternoon range, bottoming at 4,127.7, within two points of the day's first computed support at 4,129.0, where responsive buyers lifted it back toward 4,150. The candle reads as a failed retest of Monday's breakout, and it stalled at the one average that has capped this recovery from below.

The June low at 3,955 is the level the entire five-day recovery is built on, and we have flagged it as the structural base in every gold note since it formed. The past week's 110-point rebound is the strongest stretch since that low printed, worth about 2.72 percent, and it carried price back above the 5-day average and straight into the declining 20-day at 4,178.8. That is where sellers live. With tomorrow's FOMC minutes as the week's dominant event and dealers positioned to amplify whatever starts, today is a decision inside a still-broken market.

Three stages, one basing attempt

Price sits in roughly the 31st percentile of its 52-week range, 3,441.5 to 5,706.0.

Monday was the bulls' day: the contract rallied from the prior weekly close near 4,125.7 to settle 4,167.5, with the week's high at 4,215.5 before sellers appeared. The overnight reversal digested that between well-defined edges, session volume through the European morning about 33,400 contracts with open interest near 274,200. The daily downtrend sequence of lower highs stays intact until the June 17 swing high at 4,403.6 goes; Monday's 4,215.5 rejection put in a fresh lower high against the late-June swing. On the 4-hour chart the June-July recovery is a sequence of higher lows off 3,955.4, and the current bar opened 4,142.4 grinding toward 4,148. A change of character for the bulls requires a 4-hour close above 4,180; for the bears, a decisive close below 4,127.

The average stack tells the trend bluntly. Spot near 4,147 sits above the 5-day (4,112.6) but below the 20-day (4,178.8), the 50-day (4,439.3), the 100-day (4,696.5), and the 200-day (4,552.3). Note the inversion, the 100-day sits above the 200-day, a legacy of how violent the first-quarter markdown was. The 9-day crossover stalls near 4,149.4, essentially where the market hovers now, and the 18-day reference at 4,163.4 sits inside today's supply band. The 40-day at 4,386.7 is the medium-term line the recovery would need to reach before anyone can argue the trend has turned. Momentum has recovered from the June washout without flipping constructive: the 14-day relative strength at 42.52 is below the midline but off oversold, the 9-day raw stochastic at 74.4 percent is short-term stretched after the bounce while the 14-day (43.2 percent) and 50-day (22.4 percent) stay subdued. The directional index reads a strong 38.0 with the down-line (24.5) still dominating the up-line (15.2), so the prevailing daily trend remains down and strong. The composite reads 80 percent sell, 60 percent short-term, 75 medium-term, 100 percent long-term; the only buy in the stack is the 10-8 day hi-lo channel reflecting the recent bounce.

A dealer environment with no brakes

Dealer positioning is read through the gold ETF proxy, which trades near one-tenth the futures price, so proxy levels translate at roughly 10.85 to 1. The most recent model update is dated July 3, the proxy last marked 382.15 against a prior close of 378.11. The standout feature: both call gamma (negative 116 million) and put gamma (negative 183 million) are net negative, meaning dealers are short options exposure on both sides and their hedging amplifies moves rather than damping them. Momentum in either direction begets more of the same, consistent with the 52-point overnight swing. The high-volatility inflection on the proxy sits at 361 (roughly 3,915 in futures terms), well below the market, and the low-volatility reference is far beneath at 297. Between here and 361 the environment stays amplified; there is no dampening zone anywhere near current prices.

"Expect exaggerated intraday swings, respect momentum once a level breaks, and treat the 4,123 to 4,231 translated band as the magnetic zone."

Strike concentration on the proxy runs through the 380 to 390 band, which translates to approximately 4,123 to 4,231 in the futures, bracketing today's expected zone almost exactly. The largest gamma expiration is July 17, so this amplified environment persists through the week. The options-implied daily move on the proxy is about 5.5 dollars, roughly 1.4 percent or 60 futures points, and with one-month realized volatility (31.5 percent) running well above implied (23.1 percent), the options market is arguably underpricing the metal's actual travel; implied rank is moderate at 32 percent. On the speculative side, call open interest meaningfully outweighs puts on the proxy, a put-call open-interest ratio of 0.61, and Monday's call volume ran nearly double put volume, so the crowd is still leaning toward upside exposure even as trend systems remain uniformly short. That divergence, retail optimism against systematic selling, is characteristic of a market working through a base.

A two-sided macro, a safe-haven bid that will not quit

The dollar remains the largest long position in G10 currency markets, but bank positioning trackers flagged fresh selling interest last week, a mechanically supportive development for gold. Rates are the tension point: Thursday's payroll miss (57,000 against 113,000) dragged the front end dovish, but the June projection materials showed half the committee entertaining a 2026 hike, and today's 1:00 PM ET 3-year note auction (last stop 4.192 percent) plus tomorrow's minutes steer the real-yield conversation. Japan's 30-year auction overnight drew the strongest demand since 2019, calming one corner of the global duration anxiety that had been feeding hard-asset demand. Governor Bowman's remarks at 7:00 AM ET were the first Fed voice of the session, and the inflation pulse runs through second-tier prints this week, the 11:00 AM ET New York Fed consumer inflation expectations today, Chinese prices tomorrow night, Japanese producer prices Thursday. June PCE at 0.4 percent monthly kept the disinflation narrative alive without settling it.

The Middle East is the market's live wire. Overnight, Germany's foreign minister said in Israel that Iran must guarantee free passage through the Strait of Hormuz, witnesses reported explosions in Damascus, and Saudi Arabia is holding preliminary talks with neighbors about moving crude around the strait entirely while weighing pipeline expansion to the Red Sea coast. The late-June sequence has cooled but not resolved, and the NATO summit convenes in Ankara today. Each keeps a residual safe-haven premium under bullion, and any re-escalation headline is an immediate upside catalyst regardless of the technical picture. Cross-asset, equities enter cautious after the Bank of England warned that the risk of a sharp correction remains high with valuation stretch beyond the AI theme, remarks that landed alongside a 1 percent Nasdaq-100 decline; the yen firmed modestly after repeated suspected interventions, crude is bid about 1 percent on the Hormuz story, a tailwind for the inflation-hedge bid, and no fresh official-sector purchase data crossed overnight. Official-sector accumulation was a pillar of the 2025 advance, and the question since the January peak has been the pace, not the direction, of that demand.

The trade: fade strength into supply

Overnight rejection printed exactly at the 20-day average and four-week 50 percent retracement confluence; the 4,163 to 4,180 band stacks the prior settle, the daily pivot at 4,172.3, and the 18-day and 20-day averages into one supply shelf, and amplified dealer positioning rewards momentum once the band rejects. Short 4,163 to 4,178 on evidence of stalling, a failed 15-minute reclaim of the pivot or a first lower high after tagging the band. Stop 4,192, above the pivot, the 20-day, and the overnight high with buffer. Targets 4,129 (first pivot support and overnight-low shelf), then 4,115 (one-standard-deviation, 5-day zone), then 4,092 (second pivot stack), roughly 1:1.6, 1:2.2, and 1:3.0 from a 4,166 average entry. Two consecutive 15-minute closes above 4,180, or any 15-minute close above 4,192, flips the intraday structure and cancels the fade.

The alternate is the responsive-buyer trade at the shelf that already held once overnight: if price breaks below 4,127.7, flushes toward 4,115, and then reclaims 4,129 on a 15-minute close, enter long targeting 4,150 then 4,167, stop below 4,112. It demands the reclaim, never anticipation. Skip the session if price gaps above 4,210 at the open, if it opens below 4,090 (trend-day risk in an amplified environment), or if a major Hormuz or Fed headline lands inside the first 30 minutes and produces a straight-line move. Reduce size across the board ahead of tomorrow's 2:00 PM ET minutes; this is a positioning day, not a conviction day. Any Strait of Hormuz escalation headline voids all short setups immediately, safe-haven flows overwhelm technicals in this environment.

Today's calendar (ET). A second-tier data day; the week's gravity is tomorrow's minutes.

A decision zone with supply overhead and a once-tested shelf below, in an amplified dealer environment, ahead of a next-day policy event.

Dovish data lifts it, hawkish rhetoric caps it. That is a market coiling under its 20-day, waiting for the minutes to pick a side.

The complete data picture

Every level and reading from the morning gold review, in full.

| Resistance (bottom to top) | Support (top to bottom) |

|---|---|

| 4,163.4 to 4,167.5 18-day reference, Monday settle | 4,127.7 overnight low; 4,129.0 first pivot support |

| 4,172.3 daily pivot | 4,115.3 one-SD support |

| 4,176.4 to 4,179.5 overnight open/high, 20-day 4,178.8, 50% retrace | 4,112.6 rising 5-day average |

| 4,210.7 first pivot resistance, 4,215.5 Monday high, 4,216.9 target | 4,090.6 second pivot support; 4,093.7 two-SD band |

| 4,219.7 one-SD, 4,241.3 two-SD; 4,254.0 second pivot; 4,292.4 third pivot | 4,047.3 third pivot support |

| 4,403.6 June 17 recovery high (caps the bigger picture) | 3,955.4 June low base; 3,920.8 secondary reference |

Moving averages: 5-day 4,112.6, 20-day 4,178.8, 50-day 4,439.3, 100-day 4,696.5, 200-day 4,552.3 (100-day above 200-day inversion), 9-day cross 4,149.4, 18-day 4,163.4, 40-day 4,386.7. Range: peak 5,706.0 (Jan 29), -27.3% since; 13-week extremes 4,953.8 to 3,955.4; 52-week range 3,441.5 to 5,706.0. Proxy (July 3 update): marked 382.15 vs 378.11; high-vol inflection 361 (~3,915 fut), low-vol 297; strike concentration 380-390 (~4,123 to 4,231 fut); largest gamma expiry July 17; implied daily move ~$5.5 (~1.4%, ~60 fut pts); translation ~10.85:1.

Intraday prints: Monday settle 4,167.5 (+~1.0%), week high 4,215.5; overnight open 4,176.4, high 4,179.5, low 4,127.7, near 4,147, volume ~33,400, open interest ~274,200; overnight burned 52 points; current 4-hour bar open 4,142.4. Expected range: low 4,090 to 4,115, mid 4,127 to 4,185, high 4,210 to 4,220; one-ATR band 4,051 to 4,284; ADR envelope 4,058 to 4,277. Paths: A 45% (fade at supply, retest 4,129); B 30% (reclaim 4,172 with acceptance, squeeze toward 4,210); C 25% (early break of 4,127.7, extension into the 4,090s). Setup: short 4,163 to 4,178, stop 4,192, T1 4,129, T2 4,115, T3 4,092, R:R 1:1.6 / 1:2.2 / 1:3.0. Alternate: long a sweep-and-reclaim of the overnight low, break below 4,127.7, reclaim 4,129 on a 15-minute close, targets 4,150 then 4,167, stop below 4,112. Macro override: any Strait of Hormuz escalation voids all short setups. Calendar (ET): 7:00 Bowman; 8:30 US and Canada trade balance; 10:00 Canada Ivey PMI; 11:00 NY Fed inflation expectations; 12:00 energy short-term outlook (tentative); 1:00 US 3-year note auction (prior 4.192%); 10:00 PM New Zealand rate decision (2.50% consensus); Wednesday 2:00 PM FOMC minutes.

A five-day bounce meets its 20-day ceiling.

See how AlgoIndex turns this kind of read into systematic signals. Read today's crude note and the pillar on how volume-profile levels are built and tested.

View pricing