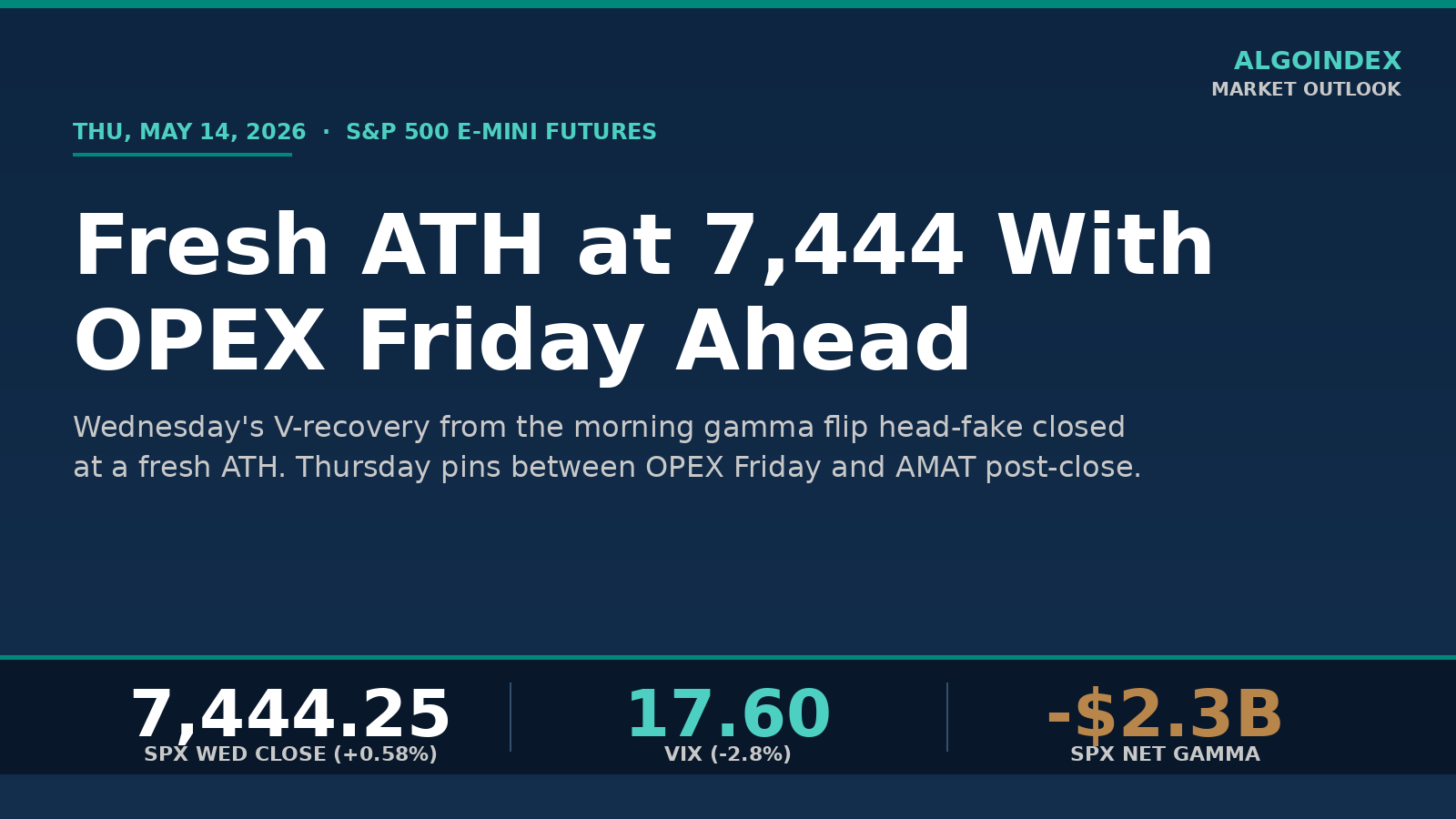

At 9:38 AM Wednesday, S&P 500 E-mini futures bottomed at 7,407, twenty-three points below the open and right at the strike where dealer hedging had been pulling sellers down overnight. Eight minutes later the index was back at the open. By 2:30 PM it printed a fresh all-time high at 7,460 cash, and by the close the S&P 500 had added 43 points to settle at 7,444.25.

The morning's drop looked like a "sell-the-news" reaction to the 8:30 PPI print. It was something else. Producer prices for April came in at 4.0% year-over-year against a 4.8% forecast, eighty basis points cooler in a single release, the kind of dovish surprise that usually sends equities straight up. Instead, real-time options-delta data showed a negative print of $882 million in the first eight minutes, the day's extreme, driven almost entirely by 0DTE put-side hedging at the 7,400 strike. Once that mechanical noise exhausted, the same hedge desks were forced to buy back the other direction. The afternoon's cumulative-delta swing of nearly $9 billion is what carried the price action from 9:38 trough to 2:30 high.

That structural recovery sets up a specific Thursday. Cooler producer prices and Kevin Warsh's mid-day Senate confirmation as Fed Chair removed two layers of policy uncertainty in a single session. Implied volatility crushed nearly three percent on the day to 17.60. Net dealer gamma still sits at negative $2.3 billion, which means any fresh catalyst gets amplified, but the immediate setup favors pin behavior between Wednesday's close and Friday's monthly options expiration. The iron level is the multi-framework confluence at SPX 7,393 to 7,400, where computed pivot levels intersect with options-flow data and Tuesday's close, all stacked. Above it, the bull structure stays intact through Friday. Below it, the thesis breaks.

How an opening dud became a fresh all-time high

The opening sell-off was real but shallow. ES dropped twenty-three points in eight minutes, then took fifty-seven minutes to fully reclaim the open. The recovery was not retail dip-buying. Order-flow data showed aggressive iceberg orders absorbing every offer between ES 7,410 and 7,413, with single-print sizes of 446, 376, and 367 contracts hitting the bid in succession. Cumulative volume delta on the futures book pivoted from positive 1,000 to positive 1,808 by 10:35 ET, then rocketed to 5,501 by mid-afternoon as the mechanical hedging chain compounded.

Two macro inputs amplified the move. The PPI miss reset the inflation conversation that Tuesday's hot CPI print had broken, and Warsh's confirmation removed the policy-overhang risk that had been priced into yields all week. Treasury yields eased about five basis points across the curve, the dollar index slipped 0.17 percent, and the semiconductor complex recovered the entire previous-day drop. The chip-sector ETF added 2.06 percent, the 3x semi product bounced from a 9.4 percent loss the prior session, and large-cap tech leadership reasserted itself across NVDA, AAPL, and TSLA. Yesterday we mapped the same dealer-mechanic pattern in the 7,400 gamma-flip article; today's fresh-ATH close confirms that thesis ran the full course.

The session's only real warning sign came in the final ninety minutes, when futures cumulative delta rolled to negative 4,803 while price held at the high of the day. That is the standard signature of distribution into retail buying at the top, and it caps the immediate upside, but it did not trigger a sell-off because positive gamma support absorbed the flow. The implication for Thursday is bounded upside near the 7,475 to 7,500 zone, not an immediate reversal.

What the gamma-flip recovery actually changes

BEAR

LEAN

BULLISH

The 7,400 strike that flipped to negative gamma overnight Tuesday reclaimed positive territory by Wednesday's close. The mechanic is now inverted from yesterday's setup. Above 7,400, dealer-positioning data shows positive gamma extending upward, which dampens intraday moves and pulls price toward the larger gamma concentration strikes. Below 7,400, negative gamma still amplifies any selling, and the iron level sits at SPX 7,393 to 7,400 where the computed first-pivot support from Wednesday's range overlaps exactly with the options-flow pivot.

The dealer-positioning stability read closed at roughly 75 percent, in the upper half of its range, which corresponds to a pin-and-grind day rather than a trend day. The forward-vol-of-vol gauge slipped to 96, also lower, consistent with continued suppression through Friday. The cumulative options-delta band still shows mild negative bars into the close, which is consistent with capped upside but not breakdown.

The single most important reading from the real-time hedging-flow exec summary is the SPX net gamma at negative $2.3 billion. Dealers remain short gamma, which means any fresh catalyst gets amplified in either direction. The setup is calm by default, but volatile if a binary headline lands.

Thursday's iron pivot and the primary setup

The decision matrix at 9:45 ET is short. ES holding above 7,460 with the morning data digestion clean fires the long-pullback trade. Entry sits in the 7,460 to 7,470 zone, stop at 7,448 (just below the SPX 7,418 first-support shelf), first target at 7,488, second at 7,500, third at 7,510. The risk-to-reward on the first target runs roughly 1:2.3, the third stretches past 1:4.

ES opening below 7,440 with implied volatility re-expanding above 18 fires the opposite trade. The negative-gamma profile would then work against the late-week grind, with a cascade running first to 7,420, then 7,395, with the 7,395 break being the first real conviction-bear signal. The structural lower pivot at SPX 7,290 to 7,308 only matters if 7,395 breaks decisively. Our performance methodology documents how we filter waiting-window rules per data tier.

There is no first-tier US data release on the order of FOMC, CPI, payrolls, or core PCE today, which means the standard 15-to-30-minute post-release waiting requirement does not apply. The catalyst stack is still heavier than the macro tier suggests, and one specific item shapes the next two sessions.

The catalyst stack: 8:30 dump, VIX settle, AMAT after the close

April Retail Sales, jobless claims, and two regional Fed manufacturing surveys all release simultaneously at 8:30 ET. None individually moves the index more than 25 basis points on consensus, but the combined read is the consumer-pulse update for the week. Stronger numbers extend the bullish-into-OPEX setup directly. Soft retail brings back rate-cut-pricing concerns and pulls the index toward the 7,420 magnet.

The VIX cash settlement at 9:30 ET is a procedural event that nonetheless creates noticeable open-print noise for fifteen to thirty minutes. The Iron Rules already block entries during the 9:30 to 9:45 window, but on VIX settlement days the internal-breadth readings often whip on the first two five-minute candles. We do not trade those candles.

The single largest catalyst for the next two sessions is Applied Materials reporting after the close. AMAT runs the semi-capex narrative that rhymes with NVDA's 5/20 print, and any miss could spill into Friday's open with the entire chip-cycle thesis under pressure. AAPL put buying surfaced in Wednesday's exec summary at approximately negative $352 million in delta terms, which is consistent with specific Mag7 hedging into the AMAT print and the NVDA event next week. The same dealer-positioning framework anchored the 7,232 call-wall fade in late April; the friction strike has now climbed to 7,500.

The week's structural pivot remains Friday's monthly options expiration, when the gamma profile rolls and the suppression mechanic that has held volatility low for two weeks finally releases. The post-OPEX direction depends on the AMAT and NVDA reactions more than on tomorrow's intraday price action.

The compressed-volatility environment keeps tightening; the move that follows OPEX will be larger than the recent dailies have suggested.

AlgoIndex turns this same level work into automated entries, sizing, and exits across ES, NQ, GC, and CL.

View pricingFoundational guides

New to S&P 500 futures? Start with What Are ES Futures, the ES, NQ, MES & MNQ point value and contract specs, gamma exposure (GEX) explained, and market internals: TICK, ADD, VOLD and VIX.