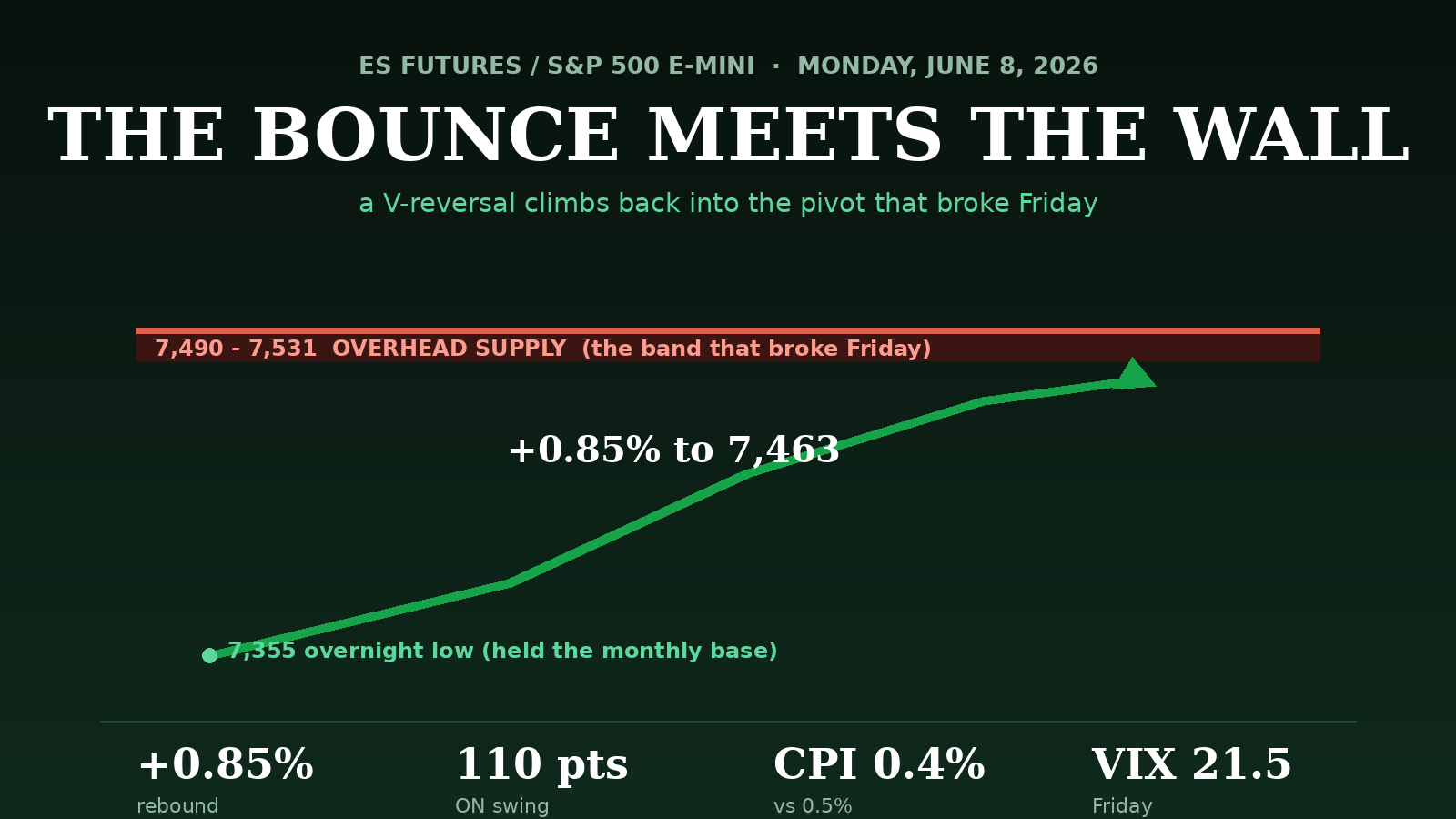

On Friday, a hot payrolls print handed the S&P 500 its worst day since April 2025, and the index closed at the lows roughly 127 points below the dealer pivot that had been holding it up. The reflex bounce that kind of high-velocity break usually produces has now arrived. The E-mini enters Monday near 7,463, up about 0.85 percent from Friday's 7,400.50 settle after an overnight session that swept 110 points from a low of 7,355.50 to a high of 7,467.75. The catalyst is a decisive turn toward geopolitical de-escalation, reinforced by a cooler inflation read. But the rebound is climbing straight back into the exact band that broke on Friday, at the exact moment dealers are still positioned to amplify moves rather than absorb them. The whole session comes down to one level.

The V-Reversal Off the Monthly Base

Friday closed ugly, a technology-led rout that took the Nasdaq down nearly 4.8 percent and semiconductors close to 9.7 percent as a stronger-than-expected employment report pushed rate expectations in a more restrictive direction. Into Monday the picture inverted. Overnight futures bottomed at 7,355.50 in the early hours, tested the monthly base almost exactly, and then rallied steadily on the de-escalation news to tag 7,467.75. The detail that matters: the cash session opened at 7,368.00, which means the bulk of the advance came after the open rather than as a thin pre-market spike, a sign of genuine demand absorbing supply rather than a hollow gap.

The driver behind the turn is a decisive shift in the geopolitical picture. Reports through the weekend and into the morning point to an Israel-Iran ceasefire framework, an announced end to military operations, the lifting of a naval blockade, the reopening of shipping lanes, and progress toward a United States-Iran memorandum pending final sign-off. The market read it as risk-on: equities firmer, energy weaker, defensive havens easing. That impulse is reinforced by this morning's cooler monthly core price index, 0.4 percent against a 0.5 percent expectation and down from 0.7 percent prior, which softens the inflation worry that drove Friday's rate shock and gives equities room to rebound. The standing risk is symmetrical: any of these reports being walked back would reverse the move just as fast, given the dealer posture overhead.

Climbing Back Into the Wall It Broke

Here is the structural contradiction. On Friday the index broke below the dealer pivot near 7,490 cash, which flipped dealer hedging into a posture that amplifies directional moves rather than absorbing them, and lifted the volatility index to 21.5. Today's rebound is climbing right back into that pivot, and into a tightly stacked band of short-term moving averages sitting just above it. Net dealer positioning is still negative, call-side near 102 million against put-side near minus 412 million, which means follow-through can be fast in both directions once a level breaks and intraday reversals can be sharp. Reclaiming the cash 7,490 area, roughly ES 7,506, is what would begin to neutralize the downside-acceleration risk. Failing to reclaim it keeps the market in the more unstable, move-amplifying environment, which is precisely why the level is the hinge of the session.

Momentum has reset to neutral, which leaves room for a move in either direction. The 14-day relative strength reading sits at 52.86, almost dead-center, and the directional indices show Friday's down-leg losing steam, the 14-day trend-strength index easing to 29.06 from an elevated short-window reading. The 14-day average true range is about 91 points, so centering a roughly 85-to-95-point band on 7,460 frames a likely session of about 7,375 on the low side to 7,550 on the high side, with the caveat that an unstable dealer environment can stretch either tail.

Three Ways the Session Resolves

The data slate is light, the NY Fed inflation-expectations survey at 11:00 ET the only notable item and a secondary mover, which leaves geopolitics and momentum in control. The week's defining release is Wednesday's consumer price report, the event that will either confirm the disinflation hint or reignite the rate-hike narrative. Within today, three paths, all hinged on the 7,490 pivot.

The Setup: Buy the Pullback, Not the Wall

The larger uptrend is intact, the monthly base held on the overnight test, and a genuine risk-on catalyst is driving the rebound. But chasing straight into the 7,500 to 7,531 overhead band with a move-accelerating dealer posture is poor risk. The higher-quality entry is a pullback that holds the 7,450 pivot or the 7,430 area, positioning for the reclaim of the cash 7,490 pivot rather than buying into it.

The rebound is real, the monthly base held, and the inflation hint is constructive. But the market is climbing back into the precise level whose loss caused Friday's acceleration, with dealers still positioned to push rather than cushion. Reclaim and hold the pivot and the squeeze has room to the next shelves; reject from it and the gap below fills. Until the 7,490 area is back overhead on a sustained basis, the burden of proof stays with the buyers, and Wednesday's inflation report is the gate that decides the week.

Next day: the bounce held the base and coiled into a tight options box ahead of CPI, in The Box Before the Print.

\nThis analysis is for educational purposes and reflects conditions ahead of the Monday, June 8, 2026 cash open. It is not investment advice. Markets carry risk; conduct independent research before acting.

Foundational guides

New to S&P 500 futures? Start with What Are ES Futures, the ES, NQ, MES & MNQ point value and contract specs, gamma exposure (GEX) explained, and market internals: TICK, ADD, VOLD and VIX.