By 10:45 AM Thursday, the position size at the SPX 7,525 strike had grown from 26,000 to 40,000 contracts. Three hours later that strike was empty. The institutions had taken their profits and rolled the bet 25 points higher, building 28,000 new contracts at SPX 7,550. By 4:00 PM the S&P 500 closed at 7,501, exactly at the strike where market makers had built the largest gamma wall of the May expiration.

The setup for Friday's monthly options expiration is the most leveraged moment of the trading month, and Thursday's close compressed every variable into a single number. Three independent reads point in three slightly different directions. The Call Wall at SPX 7,500 is the magnet that pulled price in and will keep pulling through Friday's session, because dealers are now at maximum gamma defense exactly there. The customer roll to the 7,550 strike is the institutional bet that the squeeze continues another 50 cash points before Friday's close. And the cumulative options-delta print at negative five billion at the close is the longer-dated put protection institutions built for the post-expiration window, when Wednesday's chip-sector earnings releases the gamma compression that has held volatility low for two weeks.

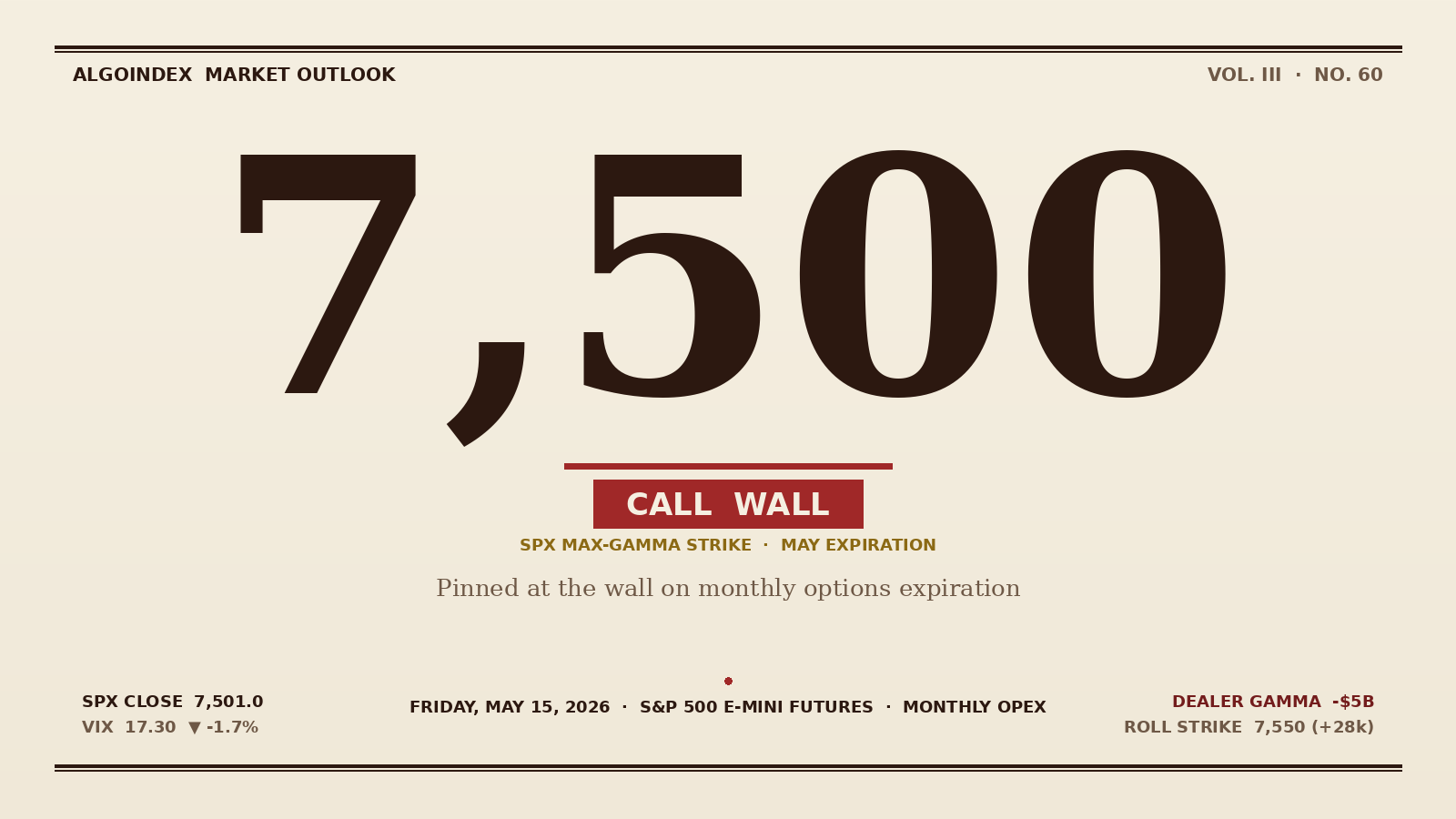

Thursday's mechanical close at the wall

The session opened with cooler-than-expected jobless claims at 211,000 against a 205,000 forecast and the previous day's PPI surprise still fueling the bid. Equity-index futures held a tight 7,485 to 7,495 range overnight on Saudi Arabia and Iran non-aggression-pact talks reported by the Financial Times, then pushed straight to ES 7,499 in the opening five minutes. The next two hours produced almost no directional movement. Volume cumulative-delta on the futures order book held flat. The pin gravity at SPX 7,500 was already in control before noon.

At 12:00 PM ET the real-time options-delta data reversed sharply. From positive three billion at midday the cumulative delta crashed to negative five billion by the close, an eight-billion swing in four hours, almost entirely driven by longer-dated put buying. That flow does not reflect bearish sentiment about Friday. It reflects institutional protection for the post-expiration window, when the gamma profile rolls and the suppression mechanic that has held the index quiet for two weeks finally releases. Dealers absorbed that put-buying and were forced to hedge it by buying the underlying, which is what produced the afternoon's clean push from ES 7,500 area to 7,520 to 7,530 zone.

The close completed the standard OPEX-week setup. The implied 1-day move for Friday is SPX 7,412.56 to 7,505.04, dealer-priced, meaning the entire expected range tops out exactly at where Thursday closed. The 99th-percentile gamma concentration moved up from 7,500 to 7,505 during the session. And the cleanest single signal of the day came in the final ten minutes, when the SPX 7,500 zero-day-to-expiration calls rose from 25 cents to a dollar. That 300 percent move in ten minutes is what a gamma squeeze looks like when dealers are short calls right at the strike.

Why the customer roll matters more than the pin

The position-rotation pattern from 7,525 to 7,550 is the smoking gun for tomorrow's upside scenario. By 10:45 AM the 7,525 strike held about 40,000 customer contracts, up from 26,000 at the open. Some hours later those positions were closed with profits, and the same desks added 28,000 new contracts at the 7,550 strike. The translation is that institutions captured the move from the 7,500 to 7,525 zone, took the gain off the table, and rolled the bet another 25 points higher.

This is not retail speculation. The contract sizes and the timing fingerprint these as professional desks. And the bet they are making is specific: it is a continuation push from the 7,500 close to a Friday close near 7,550. The Call Wall pin holding at 7,500 would invalidate the trade. The dealer mechanics actually support both outcomes, because the same hedge desks that pin the index near a strike also have to chase if it breaks above with conviction. The outcome that does not work for the 7,550 roll is the breakdown to the Put Wall at SPX 7,390, which would require something to go wrong that the entire week's price action says is unlikely.

That layered structure is what makes this OPEX particularly interesting. A pure pin to 7,500 is the dealer-favored outcome. The institutional roll says someone is betting the squeeze continues. The minus-five-billion delta close says someone else is hedging for what comes after.

Three scenarios sized to their probabilities

The decision matrix at 9:45 ET, after the special-opening-quotation noise has cleared and the opening 15-minute range has set the intraday tone, has three weighted outcomes.

Pin to SPX 7,500 carries roughly 45 percent probability. ES holds the 7,510 to 7,535 range all day, dealers defend the strike successfully, and the 3:00 PM PM-settled options drive the final hour to a close near the wall. This is the dealer-mechanics-favored outcome and the most consistent monthly OPEX pattern across the past two years.

Continuation squeeze to SPX 7,550 carries roughly 40 percent probability. The institutional position roll to the 7,550 strike is the bet structure for this scenario. ES breaks 7,535 with volume in the morning session, runs into the 7,560 to 7,580 zone by mid-afternoon, and the 3:00 PM gamma unwind produces a higher close. The trigger is a clean break above ES 7,535 with cumulative options-delta confirming the move.

Surprise breakdown to the Put Wall at SPX 7,390 carries roughly 15 percent probability. This is the tail outcome and requires a specific catalyst: hot University of Michigan inflation expectations at 10:00 ET pushing the 1-year or 5-year reading above 3.5 percent would do it, as would a Saudi-Iran deal failure or any binary headline from the still-active Trump-Xi summit window. The signature would be a break below ES 7,495 with cumulative options-delta turning deeply negative below SPX 7,485 and market-internals breadth confirming distribution.

The expected range from the dealer-priced model is SPX 7,412.56 to 7,505.04. The expected range from the 14-day average true range is SPX 7,427 to 7,575. The probable trading band that captures both reads is SPX 7,485 to 7,540, a 55-point swing centered on the pin. That band is where 75 percent of the session is likely to play out.

The OPEX-day schedule, where the volatility actually lives

Standard SPX monthly options settle AM-style at the special opening quotation at 9:30 ET. The opening print on the index determines the settlement value for the standard monthly contracts, and that print is often abnormal as the calculation methodology fires through individual constituent opens. Five to ten points of artificial noise in the first three minutes is normal on an OPEX day. The Iron Rules already block entries during the 9:30 to 9:45 window, but the rule applies with extra force during expiration sessions.

The University of Michigan consumer sentiment release at 10:00 ET is the day's only meaningful macro catalyst. The headline sentiment number rarely moves the index more than 25 basis points, but the embedded one-year and five-year inflation expectations are the data the Federal Reserve actually watches. A jump in the five-year reading above 3.5 percent would re-engage the inflation-acceleration concern that Tuesday's CPI shock briefly reawakened.

The 3:00 PM ET window is the most underrated risk on an OPEX session. The PM-settled SPXW weekly contracts and SPY Friday options expire at 4:00 PM cash, which means the gamma profile that has anchored the day rolls off in the final hour. The standard discipline is to flatten 50 percent or more of any open position by 2:45 PM. Carrying a tactical trade through the 3:00 to 4:00 PM window during OPEX is the kind of decision that produces large outcomes in either direction, and the asymmetry favors paying the spread to be flat rather than holding the position into a structure that no longer pins anything.

The primary setup and the iron level

The cleanest tradable structure for Friday is a long-pullback entry into the ES 7,500 to 7,510 zone, which corresponds to SPX 7,475 to 7,485. The stop sits at ES 7,488 (SPX 7,463), the first target at ES 7,530 (SPX 7,505), the second at ES 7,560 (SPX 7,535), the third at ES 7,580 (SPX 7,555). The reasoning is layered. The implied 1-day move's lower bound at SPX 7,412 means the primary pullback magnet is the SPX 7,475 to 7,485 zone. The institutional roll positions at the 7,550 strike provide the upside magnet for the third target. And the OPEX pin behavior favors mean-reversion entries on the long side as long as price holds above the iron level.

The iron level for Friday is SPX 7,495. The bull continuation thesis stays intact above that line. A close below ES 7,495 (SPX 7,470) breaks the call-side dealer-defense structure and opens the path to the secondary support shelf at SPX 7,450 to 7,460. A break below SPX 7,440 with volume opens the path to the Put Wall at SPX 7,390, which is the major OPEX defense level and the level the longer-dated put buyers built today's hedges against.

Position sizing returns to two or three contracts after Thursday's green session restored the discipline post-Wednesday's stop-out. No overnight carry into Saturday, since the entire week's catalyst stack rolls into Wednesday's chip-sector earnings and the post-OPEX vol expansion is what the smart money has positioned for. Yesterday's article tracked the same structural setup at the 7,400 to 7,460 confluence; today's close at 7,501 is the completed bull-week thesis that yesterday's setup forecast. Our performance methodology documents the position-sizing rules that govern OPEX-day discipline.

What this OPEX tells us about next week

The hedging-flow data points to continued equity support and volatility compression through Friday, then a transition into the following week. Wednesday May 20 brings the chip-sector earnings event that typically resets the broader index volatility expectation. Realized 30-day volatility at approximately 10 percent is the lowest reading since early February. That compressed-spring environment cannot persist indefinitely, and the institutional positioning today is consistent with the read that the post-expiration window is when the spring releases.

The strikes that matter on Friday are not retail moving averages or daily pivots. They are the levels where two hundred thousand contracts of dealer hedging flow change direction in ten minutes when the settlement moment fires.

AlgoIndex turns this same level work into automated entries, sizing, and exits across ES, NQ, GC, and CL.

View pricingFoundational guides

New to S&P 500 futures? Start with What Are ES Futures, the ES, NQ, MES & MNQ point value and contract specs, gamma exposure (GEX) explained, and market internals: TICK, ADD, VOLD and VIX.