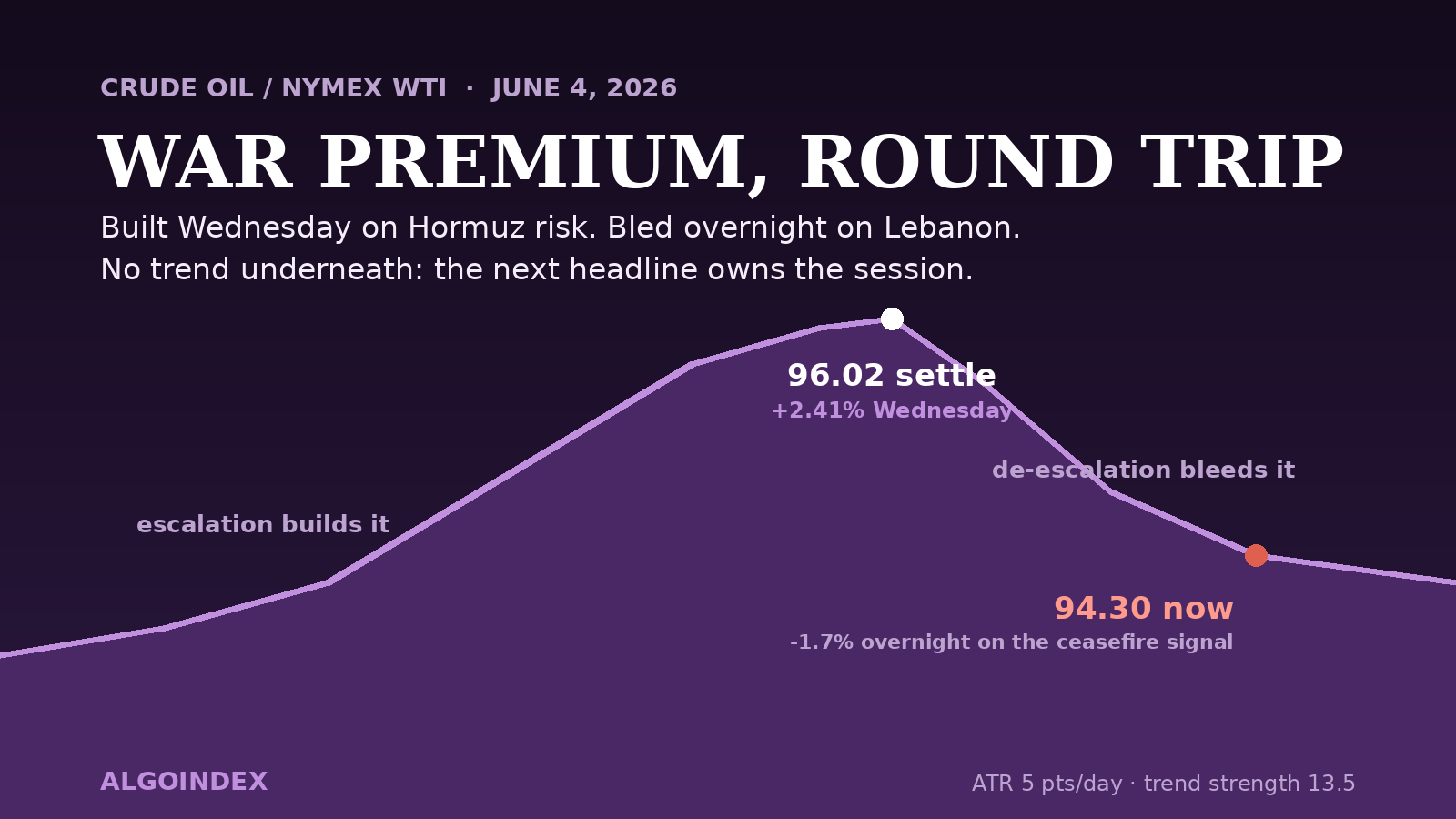

In the span of thirty-six hours, crude oil priced in a war and then priced most of it back out. Wednesday, July WTI rallied 2.41 percent to settle at 96.02, a one-and-a-half-week high, as intercepted Iranian missiles and drones aimed at Gulf states raised the odds the Strait of Hormuz stays constrained. Overnight, Lebanese officials signaled a ceasefire could begin within twenty-four hours, and the premium bled straight back out: the contract failed at 95.91, almost exactly the prior settle, and sold down to 94.06, trading near 94.30 into the early United States morning, down roughly 1.7 percent.

The speed of the round trip is itself the information. A market that surrenders nearly an entire day's advance the moment de-escalation looks credible is telling you the rally was risk premium, not demand, and premium deflates as fast as it builds. What is left underneath is a genuine contradiction: a longer-term uptrend that holds above its 50-, 100-, and 200-day averages with a five-day change still positive at 6.15 percent, sitting beneath a 20-day average and daily pivot it just lost, with trend strength so weak the directional index reads 13.5, far below the threshold that defines a trending market. Today is not a data day for crude. It is a headline day, and the headline can land from either direction.

The Premium That Built and Bled in a Day and a Half

Wednesday's advance had real fuel behind it beyond the headlines. The weekly petroleum status report showed a larger-than-expected crude inventory draw, a bullish supply signal, even as gasoline stockpiles unexpectedly built. The close at the upper end of the day's span looked constructive. Then the narrative flipped overnight: the Lebanon truce signal, an Israeli defense official suggesting the arrangement could lead to a broader agreement, and a stalled United States and Iran message exchange combined to make de-escalation credible enough to discount. The globex session opened near 95.75, rejected at 95.91 right at the settlement zone, and ground down to 94.06 on light pre-cash volume of roughly 36,500 contracts, a headline-reactive market rather than a conviction liquidation.

A Market With No Trend, by Its Own Numbers

Strip the headlines away and the technical machine says chop. The 14-day trend-strength index reads 13.50 against the 20-to-25 threshold that denotes a trending market, with the positive directional line at 22.29 only marginally above the negative at 20.21. Momentum is dead-center neutral, with the 9-day relative-strength reading at 50.63 and the 14-day at 51.11, and the stochastics sit mid-range with no extreme. The multi-indicator composite has softened to a weak 24 percent buy, rated soft and weakening, with the headline trend signal flipping to a sell. The average stack frames the same split the price action shows: spot near 94.40 holds above the 5-day at 92.73, the 50-day at 91.81, the 100-day at 80.35, and the 200-day at 70.01, but sits below the 20-day at 95.29, which together with the 95.49 daily pivot forms the short-term hurdle the whole session keys from.

The Supply and Demand Ledger Behind the Headlines

The physical story keeps a structural bid under the curve even as the acute premium deflates. Russian officials indicated the producer group does not plan to absorb the UAE's output quota, keeping that participation question open as a structural supply variable, and noted Russian production is running below its start-of-year level on unplanned refinery maintenance. The same commentary flagged roughly twelve million barrels per day of supply not reaching the market, with stockpiles drawn down to compensate for the disruption, and a diesel-export ban held in reserve as a contingency. Demand reads mixed-to-soft against that: China cut retail gasoline prices by 525 yuan per ton effective June 5 under its regular review, Canadian quarterly growth printed slightly negative, and the gasoline inventory build dragged the product leg even on crude's bullish day. The market is caught between a still-tight physical narrative and a fast-fading geopolitical premium, which is precisely the recipe for two-sided, headline-sensitive trade.

Crude carries no listed-options dealer-positioning surface comparable to the index proxies, so the positioning lens is the complex itself. Three threads matter. Term structure: the front of the curve has been supported by the disruption narrative, and a credible reopening of Hormuz flows would pressure the prompt against deferred months. The product complex: gasoline's underperformance and the contingent diesel question shape refinery run incentives through the cracks. And supply positioning: the unresolved quota issue plus lower Russian output keep the structural bid alive underneath. Sentiment caught the mood exactly, with traders described as pessimistic about an Iran deal heading into Wednesday, which is why the premium built so fast and unwound faster once de-escalation surfaced.

One Headline, Two Completely Different Days

The session's controlling variable is not the 8:30 ET jobless-claims set, which trades through the dollar and is second-order here, and it is not the 10:30 natural-gas storage report, which belongs to a different complex. It is the Lebanon ceasefire confirmation and any fresh United States and Iran or Hormuz development. The map writes itself in both directions, which is why the framework below matters more than a single-direction conviction.

→ base at 94.06 / 93.98 breaks

→ 93.59 then 93.42 retracement

deeper: 92.77 / 92.71 / 92.17 band

→ reclaim of 96.02 with momentum

→ 97.53 pivot R1 then 97.92

extended: 98.66 target · 99.04 R2

The override matrix: a single credible headline rewrites the day in seconds, in either direction. Both branches are pre-mapped.

Volatility That Demands Respect

One discipline note belongs in bold type for anyone crossing over from equities: this contract's 14-day average true range is 5.03 points, about 5.3 percent of price, with historic volatility near 52 percent. A one-range band centered on the 95.49 pivot spans roughly 90.46 to 100.52, and a four-and-a-half-to-five-point session is simply normal here. Stops sized to equity-index habits get destroyed by routine noise in this product. The practical day-range expectation absent a fresh shock is roughly 93.00 to 96.00, and even that leaves room for a two-point headline candle inside it.

Paths and the Trade

The base case, about 50 percent, is two-sided chop that fades rallies into the 95.49 pivot, holds the 94.00 base, and closes near unchanged-to-lower in the 94 handle. About 30 percent belongs to the deeper unwind, where confirmed de-escalation or a firmer dollar breaks the base toward 93.42 then 92.77. The remaining 20 percent is the squeeze, a re-escalation headline or soft dollar pushing back through 96.02 toward 97.53. The primary trade follows the fade: short the 95.49 to 95.79 pivot-and-average confluence on a rejection, stop above 96.15 where a sustained reclaim of the prior settle kills the lean, targeting 94.06, then the 93.98 to 93.59 layer, then 93.42, roughly one-to-two out to one-to-three-and-a-half. The conditional long exists only with a catalyst: above 96.15 on a fresh supply-risk headline, targeting 97.53 then 97.92, stop back below 95.49. Without that catalyst, treat reclaims of 96.02 as squeeze risk rather than trend resumption. Skip the chop inside 94.50 to 95.30, skip the fifteen minutes around the 8:30 data, and skip entirely while a major headline is actively gapping the market on every print.

We publish our performance methodology openly so every read can be measured against what it claimed. Today's companion reads cover the dealer cushion holding up the S&P, the Nasdaq's crowded-trade unwind, and gold's defense of its 200-day line, with Friday's payrolls the macro set-piece hanging over all four.

War premium is the only thing crude prices faster than it unwinds. This week it did both before Thursday's open.

Related reading: Friday's payrolls-day map for ES.

See how AlgoIndex turns this kind of read into a disciplined daily signal.

View pricing →