Follow-up: the number came in hot. See what the 172K payrolls print did to the market in Three Acts of a Selloff: ES suffers its worst day since April 2025.

\n\nOn Thursday, the Dow rallied nearly nine hundred points to a record close while the index's own generals were being sold. Capital rotated out of semiconductors and large-cap technology and into cyclicals, the broad S&P benchmark added 0.4 percent to settle at 7,584, the Nasdaq-100 lagged a full percent, and small caps gained one and a half. Strength in the average, weakness in the leadership: that is the contradiction ES carries into Friday, trading near 7,568 after a quiet overnight slide from a 7,601 settle.

And none of it decides anything, because at 8:30 ET, an hour before the bell, the May employment report prints. Consensus sits near 88,000 payrolls with unemployment holding at 4.3 percent, the rates market has been leaning hawkish enough to price a small probability of an additional rate increase this year, and overnight headlines added a fresh risk vector, Iranian naval forces firing warning shots at US destroyers in the Gulf of Oman alongside a US boarding of an Iran-linked vessel. The honest read of the morning is simple: the first hour belongs to the jobs number, not to any pre-positioned setup. Everything below is the map for what comes after it.

A Record Built by Different Hands

Thursday's internal divergence is the cleanest read in the market. The rotation out of growth and semiconductors into cyclicals, financials, and small caps kept the index aloft and pushed the Dow to a record, but it concentrated a new kind of risk: the headline benchmark is now depending on breadth rather than on its former leaders, and options activity in the mega-caps and the Nasdaq proxy has been reading extreme on the call side, a condition that caps upside and amplifies air-pockets if the leaders crack. With the Nasdaq proxy closing below its volatility inflection level while the broad index and small caps held above theirs, the message is rotation, not broad accumulation, and that makes the breadth reaction to this morning's number more important than the index print itself.

Thursday's rotation board: a record close paid for by the index's own former leaders.

The Box the Market Drew Overnight

The overnight session compressed the question into a 44-point box: a high of 7,591, a grind to 7,546.75 in thin liquidity, stabilization near 7,568 into the European morning. That box sits inside an intact swing structure, the sequence of higher lows off the late-May base is unbroken, and the moving-average stack is bullish on every horizon except the shortest, with price under the 5-day at 7,594 but far above the 20-day at 7,507, the 50-day at 7,191, and the 200-day at 6,954. Momentum is firm without being stretched, the 14-day relative-strength reading at 63.7 and the directional index at 31.3 with the positive line in control, and the composite reads 80 percent buy. Structure says trend pause; the box says the market refuses to commit before the data.

What the Hedging Flow Gave Back

Dealer positioning remains net supportive, and Thursday showed both its strength and its limits. Positive dealer gamma dampened the swings, same-day put selling around the cash 7,500 strike provided support, and the 99th-percentile dealer-positioning level near cash 7,600 capped the session from above. But the real-time hedging flow told a fading story: customer delta peaked around plus six billion intraday and rolled down to finish near plus two billion, with the activity dominated by short-dated volatility selling rather than directional conviction. That posture compresses ranges and offers no fuel. The desk behind the dealer-positioning research has also flagged a cross of its medium-term correlation risk barrier and begun adding longer-dated downside hedges through July put spreads and volatility calls while keeping its core long, the signature of a market that is constructive and increasingly alert at the same time.

The flow surface frames the day precisely. Resistance layers at cash 7,550 and 7,600, the risk pivot sits at cash 7,490, constructive above and defensive below, and the dealer-positioning dampening zone sits overhead, with a lower volatility inflection point near cash 7,660 and a higher one near 7,790. Net options impact near 4.4 billion reinforces the fade-the-extremes character: absent a data shock, dealers are positioned to pull price back toward the 7,560 to 7,600 zone. A sustained move below the 7,490 cash pivot is the one outcome that flips the cushion from supportive to accelerant.

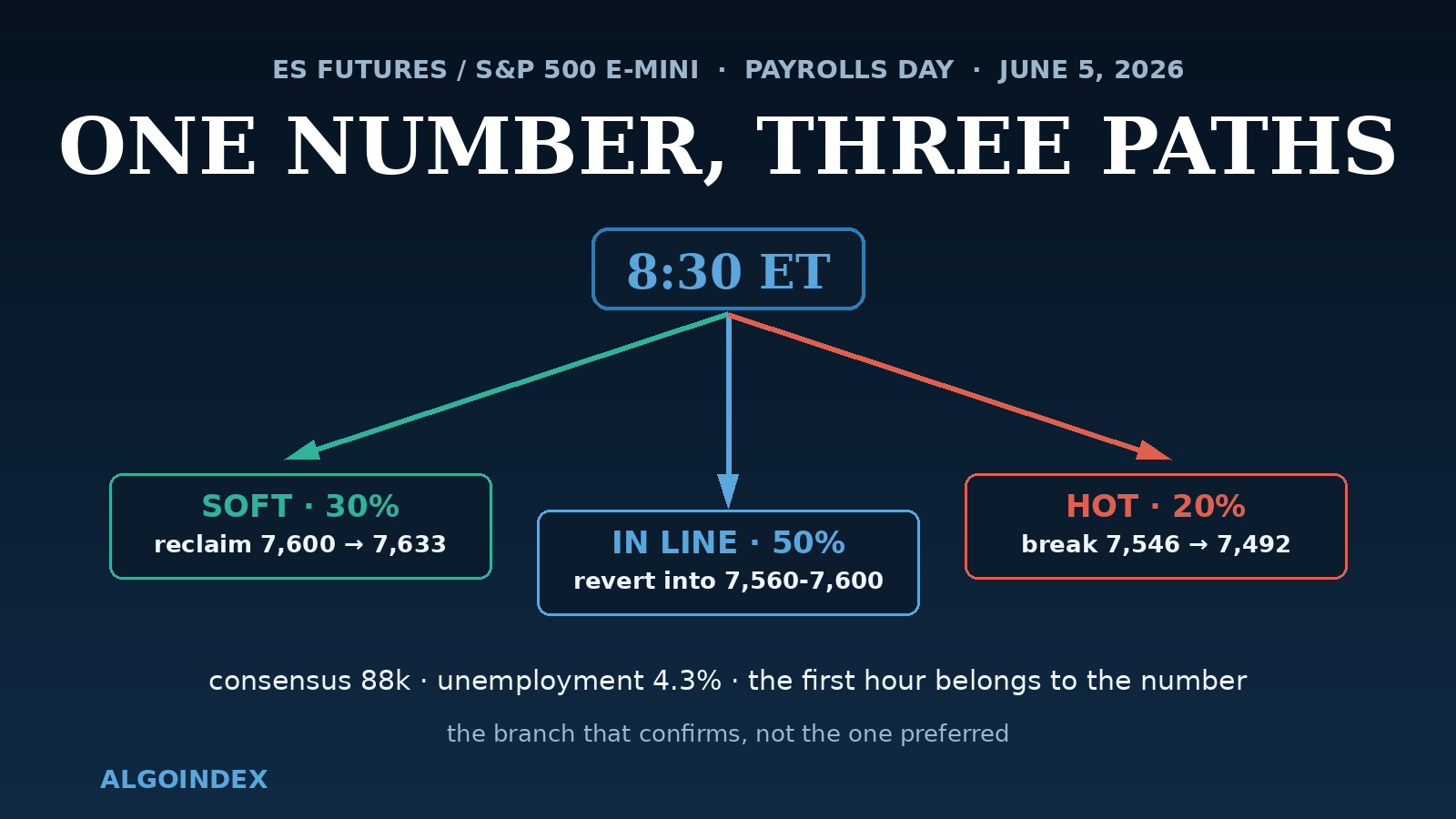

One Number, Three Paths

The reaction tree is short. A contained or in-line print, the 50 percent base case, produces a sharp 8:30 spike, a two-sided open, and mean reversion back into the 7,560 to 7,600 zone as the dampening reasserts. A soft print, about 30 percent, eases the hawkish lean, lets the index reclaim 7,591 and then 7,600, and opens a grind toward the 7,633 record. A hot print or a geopolitical escalation, about 20 percent, drives a sustained break of 7,546 and opens 7,507 and the 7,492 pivot support. The cross-asset board is already in pre-data posture, the dollar firm, the volatility gauge ticking up to the mid-15s without stress, crude near 94 with the Gulf of Oman headlines keeping a base under it, and gold slightly softer against the firmer dollar.

The reaction tree, mapped before the print. The discipline is trading the branch that confirms, not the preferred one.

The June Gauntlet Behind Today

Today's print is the first gate in a dense June slate, which is exactly why the desks are adding tail protection while staying long. The inflation print lands June 10, a mid-month central-bank decision follows on the 17th, monthly options expiration hits the 18th ahead of the June 19 market holiday, the European Central Bank meets next Thursday with a hawkish move expected, and the dealer-positioning research desk has circled a notable large-cap listing on the 12th as a potential turning point. Every one of those dates is a reason the volatility market refuses to fully relax, and a reason position size stays disciplined even on a clean setup.

The June gauntlet: five gates in two weeks, which is why desks are long with July hedges on.

The Trade: Conditional by Design

The preferred setup is a post-data, post-opening-range long: an entry in the 7,546 to 7,560 zone on a hold of the shelf and a reclaim of the 7,579 pivot with breadth confirming, a stop at 7,533 below the secondary dealer support and the overnight-low structure, and targets laddering to 7,590, the 7,600 to 7,605 ceiling, and 7,633 on acceleration, roughly one-to-two-point-six out to one-to-seven from the lower entry. The alternate is the data-shock plan, a short on sustained rejection beneath 7,546 targeting 7,507 then 7,492 with a stop above 7,563. The statistical envelope off the 14-day true range of 76.6 points frames roughly 7,491 to 7,645, and a jobs reaction can stretch it. The stand-aside conditions carry extra weight today: the setups activate only after the 9:45 ET opening range, the morning becomes a no-trade environment if the post-data range is wide and directionless or if the Iran headlines drive disorderly two-way swings, and position size shrinks everywhere because the catalyst at the open is the week's biggest.

We publish our performance methodology openly so every read can be measured against what it claimed. Today's companion reads cover the Nasdaq's overnight shelf test with the amplifier switched on, gold losing the 200-day line it defended yesterday, and crude's coil waiting on the dollar channel, and yesterday's ES read set up the cushion this number now tests.

A market this well mapped has only one honest position before 8:30, and it is flat.

See how AlgoIndex turns this kind of read into a disciplined daily signal.

View pricing →Foundational guides

New to S&P 500 futures? Start with What Are ES Futures, the ES, NQ, MES & MNQ point value and contract specs, gamma exposure (GEX) explained, and market internals: TICK, ADD, VOLD and VIX.