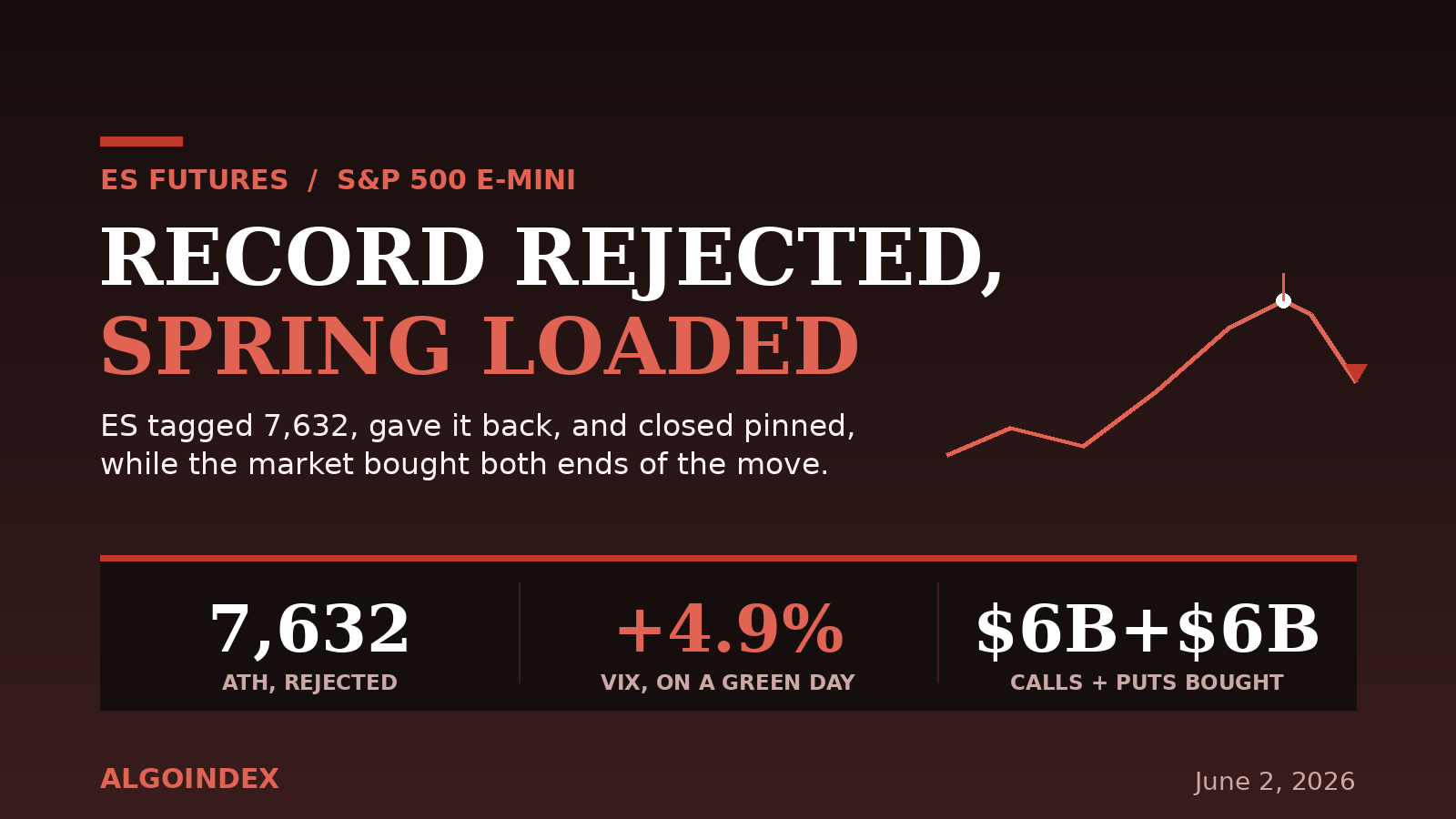

By two o'clock on Monday, ES had erased a morning flush, ripped to a fresh record at 7,632 on the back of a six percent surge in the chip bellwether, and looked unstoppable. Ninety minutes later it had given the high back. The cash index closed up three tenths of a percent, green on the day, and settled almost exactly on the 7,600 strike where the heaviest call open interest sits. A good day, on the scoreboard.

The scoreboard is not the story. Monday left a high rejection wick at a new all-time high, the first clear intraday rejection at a record in this entire nine-week run, and it did something stranger underneath: volatility rose on a green day. The volatility index closed up nearly five percent at 16.0 and the volatility-of-volatility gauge up more than six. Most telling of all, the options flow on the session was roughly six billion dollars of call buying and roughly six billion dollars of put buying at the same time. That is not a market making a directional bet. That is a market buying both ends of the move, positioning for a volatility expansion and not caring which way it breaks. The spring is loaded. The only open question is the trigger.

The Record That Would Not Hold

The day itself was a round trip. ES gapped lower at the open on a headline that US-Iran talks had halted, flushed straight to 7,576, and was immediately bought, with cumulative volume delta recovering hard as heavy bids absorbed the flush. From there it was a stair-step melt-up led by that one chip name and the rest of the megacaps, tagging the new record at 7,632 in the early afternoon. Then the final two hours reversed it. Price could not hold the high, faded about thirty points, and settled pinned at the call concentration into the cash close.

The daily candle that print left behind is a high-wick rejection bar that still closed green, which is exactly the kind of bar that rewards a second look. The trend is not broken. Price remains above every major moving average, still seventeen percent above its 200-day, still deep in the premium zone. But a first rejection at a new high after a relentless advance is a caution flag, and the daily oscillator near 84 has begun to roll for the first time in weeks. The melt-up engine is still running. It just stalled, visibly, at a number the whole market can see.

A Green Day That Felt Like a Warning

Strip out the close and look at what the hedging market did, and Monday reads less like a record and more like a warning. A green equity day normally bleeds volatility lower, because demand for protection falls when prices rise. Monday did the opposite. The volatility index rose almost five percent and its second derivative rose more than six, both climbing while the index they hedge made a new high. When protection gets bid on a green day, someone is paying up to own insurance into strength.

Volatility almost always falls on a green day. Monday it climbed, the signature of protection being bought into strength.

The internals said the same thing in a different dialect. Small caps lagged all session and closed at their own inflection level, a relative-weakness tell beneath the megacap-led advance. And the one-month implied correlation index closed at 6, far below the 8 reading that marks the line between calm and stress. A correlation index that low is the statistical fingerprint of extreme dispersion: single-stock call froth in a handful of names like the leading chipmaker, set against steady index hedging underneath. The few are carrying the many, and the market is paying to protect against the day the few stop.

The Coil: Buying Both Ends at Once

Here is the defining feature of this market, and it is worth stating plainly because it is unusual. The day's options flow was balanced almost perfectly between roughly six billion dollars of calls bought and roughly six billion dollars of puts bought. Traders were not leaning long or short. They were buying the move itself, both directions, which is what desks do when they expect the range to break hard and soon but cannot yet say which way.

That posture changes how you read the calm. Dealers still sit long gamma above the inflection level, and that positioning genuinely does dampen intraday moves and pull price back toward the call concentration, which is why Monday pinned and why the base case for Tuesday is more chop. But the cushion is the near-term story, not the whole story. Underneath it, the positioning is primed for a fast move, and the same dealer hedging that smooths the range today flips to amplifying the move the moment price falls through the level that anchors it. A pin held together by positioning that is simultaneously betting on its own break is not a stable calm. It is a coiled one.

The Two Lines That Decide It

For all the cross-currents, Tuesday compresses to a narrow band between two numbers. The ceiling is 7,630 to 7,632 in the ES domain, the implied-move-high and the record, the exact zone where buying flow stalled and the high rejected on Monday. Above it sit the stretch targets at 7,647 and the 7,657 extension, reachable only on a momentum break of the record. The pin is 7,613, the call concentration and Monday's close, the magnet that positive gamma keeps pulling price toward when nothing else is happening.

The line that matters most is underneath: the volatility inflection level at 7,568. Above it, dealer hedging dampens and the dip-buying behavior that has defined the entire run stays intact. Below it, that same hedging flips to amplifying the downside, opening the implied-move-low near 7,538 and then the deeper dealer support at 7,512, beneath which the larger dealer gamma flip level near 7,436 becomes the accelerated-decline path. Monday's regular-hours low at 7,576 sits just above the inflection level as the first warning, and the overnight session spent the evening basing right on that shelf.

Practically, the whole session reduces to this: 7,632 is the ceiling that already rejected once, and 7,568 is the trapdoor. The day is a pin between them until one gives.

What Is Pushing on the Coil

The catalysts are stacked. Monday's manufacturing data beat, with the headline at 54.0 against a 53 estimate and a resilient employment reading, which keeps the economy strong and the hawkish-rate narrative alive even as stocks rallied. Tuesday's first-order event is the job-openings report at 10:00 ET, the opening act of a jobs-heavy week that runs through Wednesday's private payrolls and culminates in Friday's employment report, for which the options market is already pricing extra premium into the end-of-week expiration. The policy-speaker slate is hawkish, with a voter speaking twice through the morning. The options market is not mispricing the week. It is bracing for it.

The engine under the advance is unchanged: a six percent surge in that same chip giant on a new product unveiling, the highest single-stock options flow in a month, and a dealer-gamma posture in that one name that can actually add upside volatility through hedging if it keeps rallying, the rare mechanic that could push the primed expansion to the upside rather than the downside. The marquee semiconductor name reports Wednesday after the close as the week's defining catalyst. Two headlines cut the other way after Monday's bell: a proposed eighty-billion-dollar equity raise from a top index weight, dilutive and a plausible drag on the soft overnight session, partly offset by a reported ten-billion-dollar investment in the same name from a marquee long-term holder. And the geopolitical backdrop stays unresolved, with talks halted, crude bid near ninety-four dollars on the returning premium, and active incidents across multiple theaters. The market shrugged all of it off on Monday's artificial-intelligence bid. It remains the most likely external trigger for the move the positioning is already paying for.

The Paths and the Trade

Put it together and Tuesday resolves into four scenarios, and for the first time in this run the downside outweighs the upside. The base case is still a pin-and-chop session between 7,576 and 7,630, capped at the ceiling and held together above the inflection level by positive gamma, a flat-to-small day that closes near the call concentration. The higher-conviction directional case is the downside one: a soft job-openings print, a hawkish speaker line, or a geopolitical headline that loses 7,576 and then the 7,568 inflection level, where dealer hedging amplifies the move toward 7,538 and then 7,512. The melt-up case is real but narrower, needing a clean break and hold above the 7,632 record, where that name's hedging can fuel a push to 7,647 and the 7,657 extension. And the tail is a hard geopolitical escalation that breaks 7,512 toward the deeper gamma flip level.

The pin is still the base case, but the directional odds now skew down, and the tail carries an accelerant.

The trade reads two-sided, decided at the inflection level and the ceiling. The cleaner directional setup is the downside break: a loss of the 7,576 regular-hours low and a failed retest of the 7,568 inflection level with weak internals, entering on the retest, risking back above the broken shelf, and targeting 7,555 then the 7,538 implied-move-low, with a runner toward 7,512 only if momentum and negative dealer gamma carry it. The alternate is to fade the ceiling, selling a rejection at the 7,613 to 7,630 zone when the hedging flow does not confirm new highs, targeting the pin then 7,594. The long is the lowest-quality side and belongs only on a clean break and hold above the 7,632 record, kept small, because chasing a melt-up into froth at the top of a coil is the worst risk-reward on the board.

The discipline this week is to trade smaller than usual, respect the 7,568 and 7,632 boundaries as the lines that actually matter, and let the 10:00 print and the opening range cast the deciding vote rather than pre-positioning into the coil. We publish our performance methodology openly so every read can be measured against what it claimed, and as Monday's record-highs-with-hedges read and Friday's read at the record both noted, the pin holds right until a catalyst gives the market permission to leave it. This time the market has already told you it expects one.

A market that buys both ends of the move at once is not predicting direction. It is predicting that the quiet ends soon.

Related reading: do gamma levels actually work? our live S&P 500 accuracy study.

See how AlgoIndex turns this kind of read into a disciplined daily signal.

View pricing →