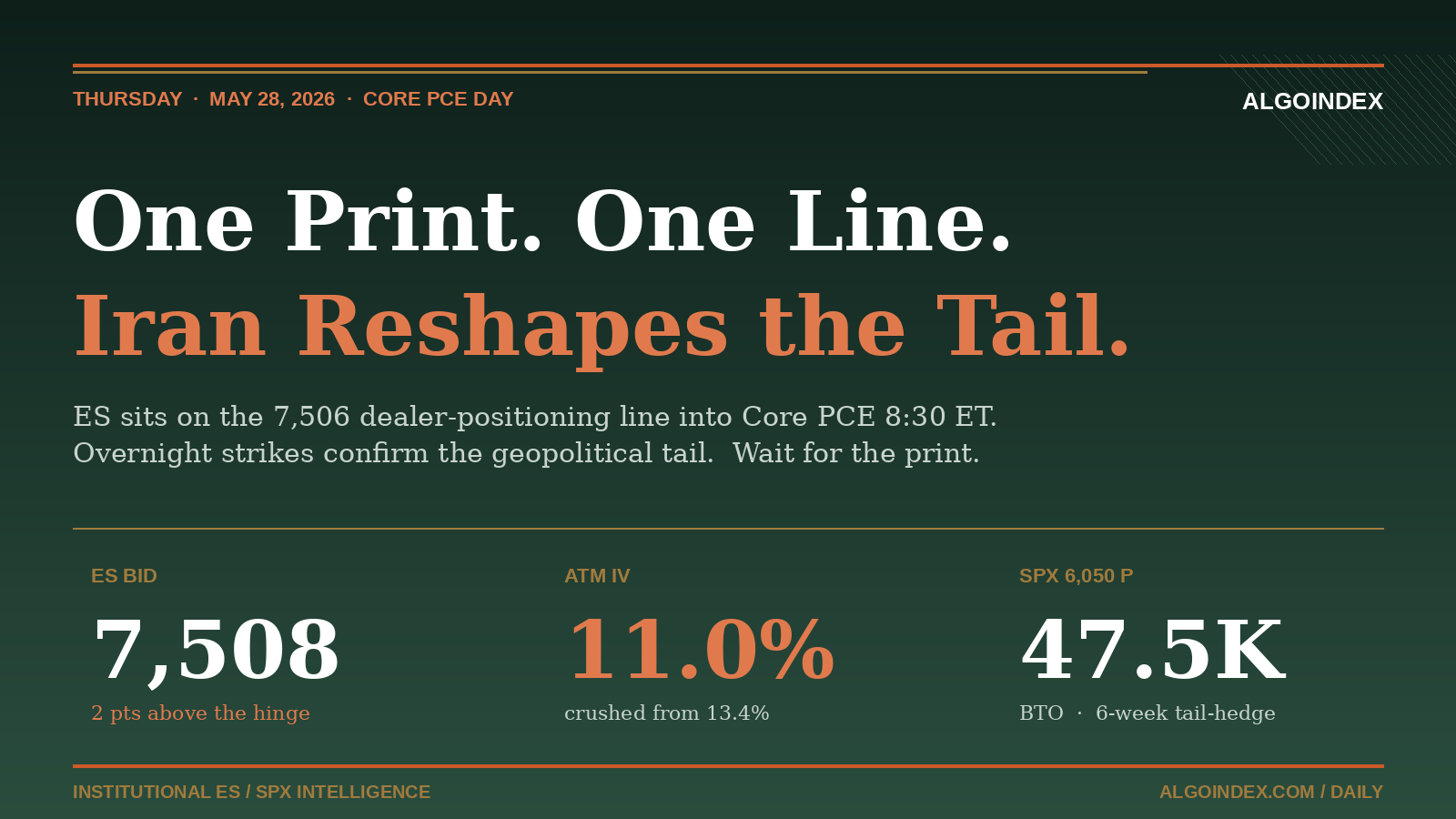

By the time the Asia session ticked into its final hour overnight, the entire weight of the holiday-shortened week was sitting on a single line. ES was bid at 7,508, drifting in a tight five-point band, and the volatility inflection level that defines the gamma-environment switch was sitting at 7,506. Two points below where price was trading. Three hours before the 8:30 ET print that resolves the calendar. And on a chart that had been rewritten in real time after the close of Wednesday's session, when a US Official confirmed that US forces had struck an Iranian military site near the Strait of Hormuz and intercepted multiple Iranian drones threatening commercial maritime traffic.

The morning that opens in front of us is built on three forces that all converge at one moment. Core PCE prints at 8:30 ET, the highest-impact data point of the cycle, with consensus 2.7 percent year-over-year and 0.2 percent month-over-month after a 2.8 prior. The Iran de-escalation framework that drove this week's risk-on rally is functionally dead after the overnight strikes, with crude bid 4.1 percent higher into 92.30 and gold reclaiming the 4,500 line. And the at-the-money implied volatility for today's option tenor closed at 11.0 percent yesterday evening, crushed from 13.4 percent on Tuesday, a level that says the options market is positioned for a muted reaction even though the news flow has done nothing but escalate the asymmetry. The trade in front of us is not a setup. It is patience. Wait for the print.

The Iran Reversal Rewrites the Week

The wire that mattered most landed long after the cash close. A US Official confirmed that the US military carried out new strikes on an Iranian military site that posed a threat to US forces and commercial traffic in the Strait of Hormuz. The same statement confirmed that US forces intercepted and shot down multiple Iranian drones. Three explosions were reported east of Bandar Abbas with air defenses activated for several minutes. The head of the Iranian Parliament's National Security Committee responded that Tehran will not retreat from its red lines on uranium enrichment, Strait of Hormuz authority, and sanctions removal. The draft ceasefire framework that drove the Tuesday gap-up and pinned the index near a fresh cycle high through Wednesday is, in practical terms, dead.

The cross-asset response was already in motion before the strikes were reported. Crude rose 4.1 percent in the late-RTH session from 88.69 to 92.32, then extended further on the strike headlines. Gold closed up 0.6 percent at 4,481 and is bid above 4,500 in the Asia session. The dollar index is mildly higher at 99.30. Ten-year yields fell to 4.39 percent on Wednesday and dropped another four basis points overnight as risk-off rotation accelerated. Bitcoin is unchanged near 76,500, which on a normal day would suggest crypto absorbing the safety bid, but in this context simply reflects that geopolitical premium is rotating into hard assets and bonds, not digital ones.

The Institutional Hedging Trade

The most important number out of Wednesday's options session is the cumulative real-time hedging flow finishing at minus 8 billion dollars, driven by 8 billion of put buying and 3 billion of call selling, with the bulk concentrated in the same-day expiration window. Historically a minus 8 billion print is a mean-reversion signal because the absorption that creates it forces dealer flow back the other way over the following one-to-three sessions, but no reversal materialized into the close because the overnight escalation removed the catalyst that any squeeze would have needed.

Underneath the same-day positioning, the longer-dated institutional positioning data tells a more durable story. Net delta across index ETFs sits at minus 2.44 billion dollars, in the 96th percentile of bearish positioning historically. The single largest index print of the day was 47,581 contracts of SPX 6,050 puts bought-to-open for July 10 expiration, a six-week tail hedge so far below current price that it functions as insurance against a much larger drawdown rather than a directional bet. VIX 60 calls for July 22 expiration saw 31,068 contracts bought-to-open. SPY 714 puts for June 18 added 23,932 bought-to-open. IWM 275 puts for June 5 added 27,519 bought-to-open. The composite read across the institutional positioning surface is that desks are paying for tail protection through mid-summer with an asymmetric size profile, while simultaneously writing upside calls to fund the protection rather than taking outright directional bets.

The bond market is delivering its own warning. Investment-grade corporate bond positioning shows delta in the 0th percentile and vega in the 0th percentile, both extremes, indicating bond traders are positioned for meaningfully higher yields out of the Thursday print. That positioning is consistent with a hot Core PCE outcome and is not consistent with the equity-vol crush that closed the session.

The Volatility Inflection Line

What makes today different from a standard Core PCE session is the geometry of where price closed. ES at 7,508 is sitting essentially on top of the dealer-positioning inflection level at 7,506, the structural line that, per the gamma framework, separates the dampened-move environment that has held all week from an amplified-down behavior pattern in which dealer hedging accelerates the same direction as price.

Sitting directly above current price is a 30,000-lot non-zero-day call structure parked at the 7,500 strike. The mechanics matter: market makers are long roughly 33,000 of those 7,500 calls and short 22,000 of the 7,500 puts, which means as price approaches that strike, dealers need to buy futures to maintain delta-neutral hedges. This is the primary mechanical force that defended 7,500 on three separate tests yesterday between 10:30 and 12:30 ET. It is also the level that needs to be reclaimed cleanly for any post-PCE rally to convert into a squeeze.

The vol-pricing setup amplifies the asymmetry. At-the-money implied volatility for today's tenor closed at 11.0 percent, crushed from 13.4 percent the prior evening. With the calendar carrying a tier-one data print, an unresolved geopolitical tail, and an extreme institutional hedging fingerprint, the vol crush is not a confirmation of calm. It is an underpricing of either tail. Whichever direction the data resolves, the move is likely to be larger than the vol surface implies, and the gamma response across the dealer book is the variable that determines how much of that move sustains.

What the PCE Print Resolves

Five reaction grids sit on the desk for the 8:30 ET window. A much cooler print, defined as Core PCE month-over-month at or below 0.1 percent and year-over-year at or below 2.5 percent, drives a 30-to-50 point rally on the cash open as the hedge unwind compounds into the 7,540 to 7,560 reclaim zone with the multi-day rejection level at 7,565 in play. A cooler print at 0.1 to 0.2 percent and 2.6 percent year-over-year produces a 12-to-32 point rally toward 7,520 to 7,540. An in-line print at 0.2 to 0.3 percent and 2.7 percent year-over-year produces chop in the 7,495 to 7,520 band with vega bleeding out of the surface. A hotter print at 0.3 to 0.4 percent and 2.8 to 2.9 percent year-over-year breaks 7,490 and tests 7,494 then 7,481 then 7,467. A much hotter outlier at 0.4 percent month-over-month or higher, especially if combined with hot Personal Income and Spending mix, cascades 45 to 70 points and opens the 7,440 to 7,416 corridor where the major dealer-positioning shelf for SPX 7,400 sits as the cushion of the day.

MoM ≤ 0.1%, YoY ≤ 2.5%

MoM 0.1-0.2%, YoY 2.6%

MoM 0.2-0.3%, YoY 2.7%

MoM 0.3-0.4%, YoY 2.8-2.9%

MoM ≥ 0.4%, YoY ≥ 3.0%

The cross-asset confirmation tells move in the opposite direction. Crude holding above 92 confirms the risk-off rotation. Crude rolling back under 90 says the Iran story is fading and the equity hedge unwind can compound. Ten-year yields up six basis points or more in the first fifteen minutes is hot-PCE confirmation. Yields down six is cool. Dollar index above 99.50 is hot, below 98.80 is cool. VIX above 18 means aggressive de-risking is underway and the hedges are monetizing. VIX below 15 means the vol crush wins.

The Primary Setup, Wait for the Print

The trade is not the entry. The trade is the reaction.

The post-print long setup activates only on a cooler Core PCE outcome (month-over-month at or below 0.2 percent, year-over-year at or below 2.6 percent) combined with a clean reclaim of ES 7,517 at the cash open. Entry zone is 7,517 to 7,520 on the first pullback after the initial rally, stop at 7,500 just below the dealer-positioning inflection line, with targets at 7,535 for the Wednesday session-high reclaim, 7,548 for the prior-day rejection zone, and 7,565 for the multi-day rejection level where the daily-review short setup historically activates. The reward-to-risk at the second target is roughly 1.6 to one, at the third target roughly 2.7 to one, and the squeeze tailwind from the minus 8 billion same-day hedging flow combined with the minus 2.44 billion institutional positioning gives the move structural fuel beyond the data.

The post-print short setup activates only on a hotter Core PCE outcome (month-over-month at or above 0.3 percent, year-over-year at or above 2.8 percent) combined with a failed reclaim of ES 7,506 at the cash open. Entry is 7,500 to 7,506 on the rejection attempt, which historically prints between 9:50 and 10:15 ET. Stop is at 7,520 above the 30,000-lot 7,500 call structure. Targets are 7,486 for the second pivot support, 7,463 for the two-standard-deviation downside, and 7,440 for the indicator support that lines up with the one-standard-deviation Pivot S2 zone. The reward-to-risk at the second target is 2.4 to one, at the third 3.4 to one, and the hot-PCE outcome plus a lost 7,490 structural pivot puts the gamma-environment into amplified-down behavior with dealer hedging accelerating the move.

Skip the trade entirely if Core PCE prints in line and ES chops in the 7,495 to 7,520 band for the first 30 minutes after the cash open. Skip if the Williams remarks at 8:55 ET contradict the directional read from the data. Skip if a fresh Iran headline produces a spike pre-print that elevates the premium above clean reward-to-risk math. Skip if order-flow analytics show mixed absorption with no clear directional pattern at the 7,506 retest. Position size is half normal across both directions, the iron rule of no entries before 9:45 ET extends to fifteen minutes past the 8:30 print regardless of how decisive the data looks in the first minute, and the 15:58 ET force-close on every same-day option remains the hard exit.

The setup is not the entry. The setup is the patience.

Foundational guides

New to S&P 500 futures? Start with What Are ES Futures, the ES, NQ, MES & MNQ point value and contract specs, gamma exposure (GEX) explained, and market internals: TICK, ADD, VOLD and VIX.